In a landmark announcement on August 5, 2025, the U.S. Securities and Exchange Commission’s (SEC) Division of Corporation Finance issued crucial guidance clarifying that certain liquid staking activities and their associated staking receipt tokens (SRTs) typically do not constitute the offer or sale of securities under U.S. federal law. This highly anticipated statement from the regulatory body provides a significant degree of clarity for a rapidly expanding sector of the decentralized finance (DeFi) ecosystem, offering a potential roadmap for innovation within established legal frameworks. The SEC’s reasoning centered on the absence of entrepreneurial or managerial efforts from the parties involved in minting, issuing, and redeeming SRTs, asserting that economic benefits for token holders stem from protocol-level staking rather than third-party management. Furthermore, the agency confirmed that SRTs, while evidencing ownership of deposited assets, are not securities themselves because the underlying crypto assets, such as Ethereum (ETH), are also not deemed securities. This pivotal clarification has far-reaching implications, particularly for prominent protocols like Lido, whose operational framework and liquid staking tokens, stETH and wstETH, align squarely with the SEC’s articulated criteria.

Navigating Regulatory Waters: The SEC’s Stance on Liquid Staking

The landscape of cryptocurrency regulation in the United States has long been characterized by ambiguity, with the SEC frequently taking an enforcement-first approach that left many industry participants in a state of uncertainty. This August 2025 statement marks a notable shift, offering proactive guidance on a specific, complex area of DeFi. The Division of Corporation Finance’s pronouncement meticulously dissects "liquid staking" as a form of protocol staking where users deposit crypto assets and receive SRTs in return. These tokens serve as a liquid representation of staked assets and accrued rewards, allowing users to maintain liquidity, transfer ownership, and engage in other decentralized applications without forfeiting their staking position.

Crucially, the SEC distinguished between protocol-based liquid staking, which relies on smart contracts and self-executing code, and arrangements involving third-party custodians. In the former, the minting, issuance, and redemption of SRTs occur programmatically, minimizing the need for human intervention or discretionary control. In both models, however, the SEC emphasized that rewards and losses are reflected algorithmically, and users are intended to retain ownership of their deposited assets. The core conclusion: these activities, when structured as described, along with the offer and sale of SRTs (even in secondary markets), generally do not fall under the purview of the Securities Act of 1933 or the Securities Exchange Act of 1934. This means that participants and providers in such liquid staking arrangements are typically exempt from registering these transactions with the SEC, unless the deposited assets themselves are part of, or subject to, an investment contract.

The Howey Test Re-examined: Managerial Efforts as the Deciding Factor

At the heart of the SEC’s analysis lies the venerable Howey Test, a four-pronged legal framework derived from a 1946 Supreme Court case, SEC v. W.J. Howey Co. The test defines an "investment contract" – and thus a security – as an investment of money in a common enterprise with a reasonable expectation of profits derived solely from the managerial or entrepreneurial efforts of others. For decades, this test has been the yardstick against which the SEC evaluates novel financial instruments, including digital assets.

In the context of liquid staking, the SEC’s Division of Corporation Finance carefully applied the Howey Test, focusing intently on the "managerial or entrepreneurial efforts of others" prong. The agency concluded that liquid staking providers, particularly in decentralized, protocol-based systems, do not exert the kind of significant managerial efforts that would satisfy this criterion. Their roles, according to the SEC, are largely administrative or ministerial. This includes tasks such as facilitating deposits, withdrawals, or token issuance, and even selecting node operators. These functions are deemed insufficient to transform the arrangement into an investment contract, as they do not involve discretionary judgment over the enterprise’s success or the generation of profits. The economic benefits realized by SRT holders, the SEC reasoned, are derived from the underlying protocol-level staking mechanism itself – the automated, code-enforced rules of a Proof-of-Stake network like Ethereum – rather than from the active management or entrepreneurial skill of the liquid staking provider. This distinction is critical, drawing a clear line between passive, programmatic participation and active, profit-generating management by a centralized entity.

Furthermore, a significant element of the SEC’s stance on SRTs themselves hinges on the regulatory status of the underlying deposited crypto asset. The Division of Corporation Finance reiterated that SRTs, while acting as "receipts" for deposited assets, are not securities if the underlying assets (e.g., ETH) are not securities. This aligns with prior statements from SEC officials who have indicated that Ethereum, post-Merge, should not be classified as a security, given its decentralized nature and the absence of a central issuer or managing entity. This foundational premise—that ETH is not a security—is pivotal for the non-security classification of stETH and wstETH.

Lido Protocol: A Case Study in Regulatory Alignment

The SEC’s guidance serves as a robust validation for decentralized liquid staking protocols that have meticulously designed their operations to be programmatic, non-custodial, and free from centralized managerial control. Lido Protocol, a leading player in the liquid staking space, perfectly exemplifies the model described by the SEC. Since its inception, Lido has aimed to democratize access to Ethereum’s Proof-of-Stake mechanism, allowing users to stake ETH without the prohibitive 32 ETH minimum, the complexities of running a validator node, or the typical lock-up periods associated with direct staking.

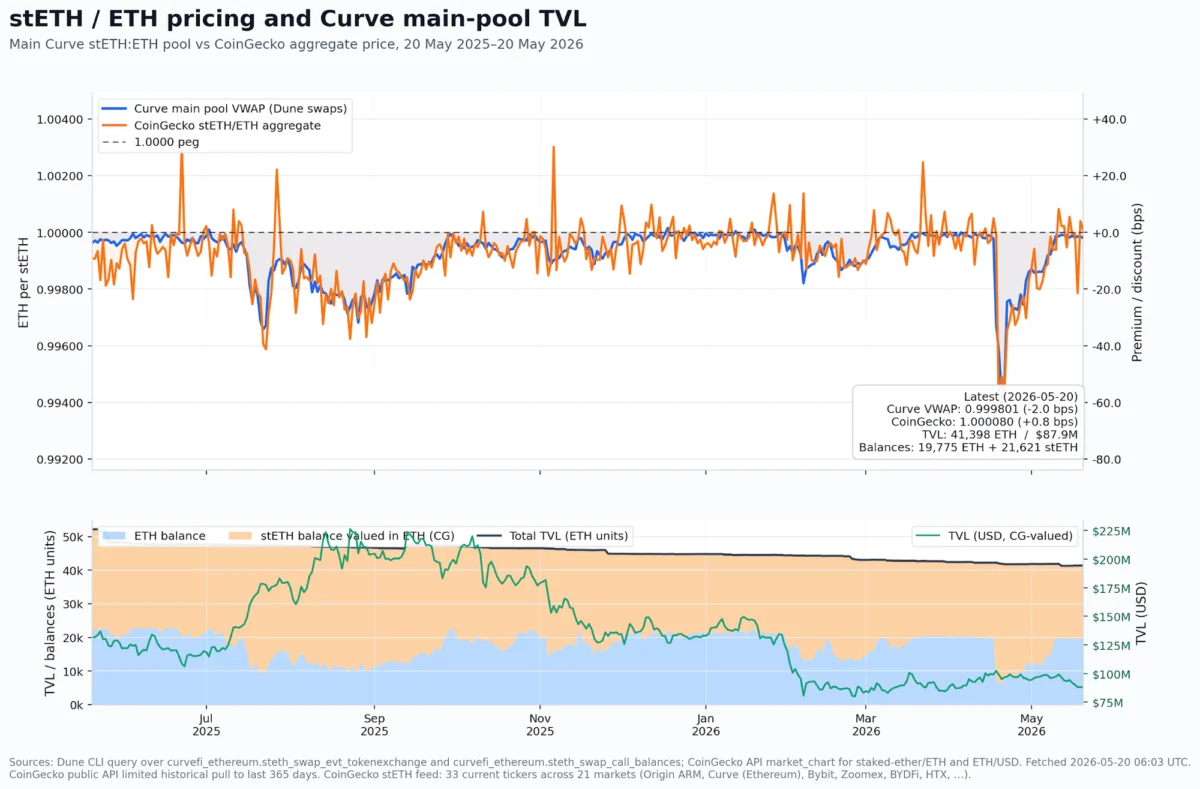

Lido’s Operational Framework: The Protocol functions entirely through a series of smart contracts deployed on the Ethereum network. Users deposit ETH directly into these contracts, and in return, receive stETH tokens on a 1:1 basis. This process of minting and issuing stETH is programmatic and autonomous, requiring no discretionary input from the Lido DAO or its contributors. Staking rewards, generated solely by Ethereum’s PoS consensus mechanism, are reflected daily in users’ stETH balances through a "rebase" mechanism. This direct, algorithmic reflection of protocol-level rewards, independent of any third-party management, aligns precisely with the SEC’s reasoning that economic benefits derive from the underlying protocol, not from entrepreneurial efforts of others.

stETH and wstETH as Non-Securities: The SEC’s statement directly addresses the nature of staking receipt tokens. stETH, and its wrapped counterpart wstETH, serve as proof of ownership of staked ETH and accrued rewards/penalties. They are not designed to generate rewards themselves but rather represent a user’s proportional share of staked ETH and the rewards earned by the underlying network validators. This distinction is crucial: the rewards originate from the Ethereum protocol’s consensus mechanism, not from any active management by Lido. The ability to transfer, trade, or use stETH/wstETH in other DeFi applications (as collateral, for lending, etc.) provides liquidity, a key feature of liquid staking, but these secondary market activities do not alter their fundamental classification as non-securities under the SEC’s guidance. The SEC explicitly states that such secondary market uses do not implicate securities registration requirements, provided the initial issuance and underlying assets meet the non-security criteria.

Governance and Decentralization: The Lido DAO, composed of LDO token holders, governs protocol-level parameters such as fee structures. However, its role is limited to administrative functions and setting overarching rules, not to the day-to-day managerial efforts that would trigger the Howey Test. The actual validator operations are performed by a diverse network of independent node operators, further decentralizing control and mitigating concerns about a centralized entity exerting entrepreneurial efforts. This governance model is consistent with the SEC’s view that such frameworks do not constitute the type of managerial efforts required to establish an investment contract.

The Rise of Liquid Staking and its Market Impact

Liquid staking has emerged as a transformative innovation in the crypto space, particularly following Ethereum’s transition to Proof-of-Stake (the Merge) in September 2022. It addresses several critical limitations of traditional staking, such as illiquidity of staked assets, high technical barriers to entry, and the significant capital requirement (32 ETH, currently valued at tens of thousands of dollars). By allowing users to stake any amount of ETH and receive a liquid representation, protocols like Lido have unlocked billions of dollars in capital, enabling greater participation in network security while simultaneously fostering a vibrant DeFi ecosystem.

Lido currently dominates the liquid staking market, with a Total Value Locked (TVL) often exceeding $30 billion and representing a significant portion of all staked ETH. This scale underscores the importance of regulatory clarity for such a critical piece of the DeFi infrastructure. The SEC’s statement is expected to instill greater confidence among institutional investors and traditional financial entities who have been hesitant to engage with crypto assets due to regulatory uncertainty. By delineating clear boundaries, the guidance potentially paves the way for broader adoption of liquid staking products and deeper integration of these assets into mainstream financial systems.

The market reaction to such clarity is likely to be overwhelmingly positive. While the specific date of the statement is in the future (August 2025), the nature of such a clarification, when it arrives, would significantly de-risk participation in liquid staking protocols. This could lead to increased capital inflows into liquid staking, further bolstering the security and decentralization of Proof-of-Stake networks like Ethereum. Other liquid staking protocols, such as Rocket Pool and Frax Finance, which operate on similar decentralized, smart-contract-driven principles, are also likely to benefit from this generalized guidance, fostering a more competitive and innovative environment.

Nuances, Caveats, and the Path Forward

While providing substantial clarity, the SEC’s statement is not without its nuances and caveats. The agency explicitly cautioned that its view applies only where providers remain limited to administrative and ministerial activities. Should providers exceed this scope, or issue tokens under different conditions that involve active managerial or entrepreneurial efforts, such activities could fall outside the purview of this statement, potentially triggering securities laws. This highlights the ongoing need for protocols to maintain strict adherence to decentralized, programmatic operations and avoid making promises of returns based on their own efforts.

Furthermore, the "unless the deposited assets are part of or subject to an investment contract" clause is a critical qualifier. This means that if the underlying crypto asset itself were deemed a security (e.g., if it originated from an unregistered security offering), then the staking receipt token representing it could also be considered a security, irrespective of the liquid staking mechanism. However, for assets like ETH, which the SEC has previously indicated is not a security, this caveat would not apply.

Looking ahead, this guidance represents a significant step towards a more mature regulatory environment for digital assets. It suggests a potential shift towards more targeted, technology-specific regulations rather than broad, all-encompassing declarations. For the DeFi sector, it could unlock a new wave of innovation, as developers and entrepreneurs can build with greater confidence, knowing that certain foundational activities are unlikely to be classified as unregistered securities offerings. The ongoing dialogue between regulators and the industry will be crucial in refining these guidelines and ensuring that regulatory frameworks evolve in tandem with technological advancements. This proactive stance, when compared to past enforcement actions, offers a more constructive pathway for the legitimate growth of the crypto economy.

Conclusion: A Milestone for Decentralized Finance

The SEC’s August 5, 2025, statement on liquid staking activities and staking receipt tokens marks a pivotal moment for the decentralized finance industry. By clarifying that these activities, when structured programmatically and without centralized managerial efforts, generally do not involve the offer or sale of securities, the agency has provided much-needed regulatory certainty. Protocols like Lido, with their transparent, smart-contract-based operations and the nature of stETH and wstETH as mere receipts for non-security underlying assets, are affirmed to align with this framework. This guidance is set to bolster investor confidence, potentially catalyze institutional adoption, and foster continued innovation within the liquid staking ecosystem, charting a clearer path for the future of decentralized finance within the U.S. regulatory landscape.

Disclaimer: This document is for informational purposes only and does not constitute an offer or solicitation to participate in liquid staking. Any decision to participate should be based solely on your own due diligence and should be made only after consulting with your own legal, financial, and tax advisors. The information contained in this document has been obtained from sources believed to be reliable, but we do not guarantee its accuracy or completeness. Past performance is no guarantee of future results. The value of crypto assets may fluctuate, and you may lose some or all of your contribution. Crypto products are unregulated and can be highly risky. There may be no regulatory recourse for any loss from such transactions. The risks associated with purchasing, storing, and trading in cryptocurrencies in general, including but not limited to regulatory, technological, and market risks, are significant and should be very carefully considered. This document is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local laws or regulations. As the Lido middleware is a decentralised software application, it is your own duty to research and understand the laws applicable to your participation in liquid staking. No financial, legal, regulatory, tax, or accounting advice.