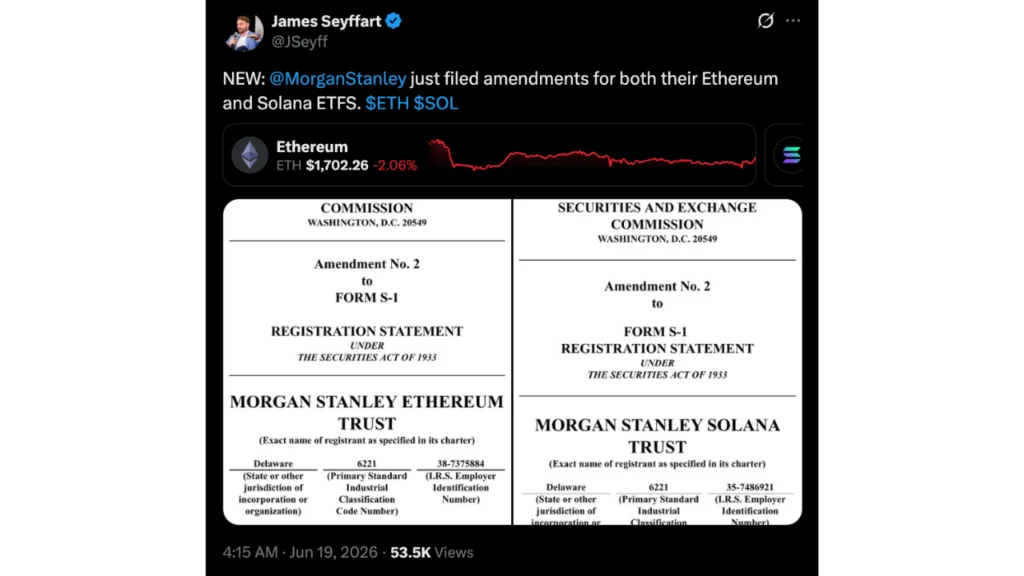

Morgan Stanley has taken a significant stride towards launching its highly anticipated spot Ethereum and Solana exchange-traded funds (ETFs), filing second-amended S-1 registration statements with the U.S. Securities and Exchange Commission (SEC) on Thursday. These updated filings are particularly noteworthy as they introduce a detailed fee structure and staking mechanism for both products, positioning Morgan Stanley to potentially offer the cheapest ETH and SOL ETFs currently available in the United States. This strategic move underscores the investment bank’s aggressive ambition to capture a substantial share of the rapidly evolving digital asset ETF market.

Second Amendment Signals SEC Progress and Active Dialogue

The submission of these second amendments for both the Ethereum and Solana ETF applications, which were initially lodged in January, is widely interpreted by market observers as a strong indicator of ongoing and constructive dialogue between Morgan Stanley and the SEC. While the regulatory body has yet to grant final approval for either fund, the iterative nature of amended filings typically reflects the issuer’s responsiveness to regulatory feedback and marks tangible progress toward a potential green light. Each revision represents a step forward in addressing the SEC’s requirements and concerns, moving the applications closer to a final decision.

The proposed Ethereum ETF is slated to trade under the ticker symbol MSSE, while the Solana ETF will be identified by the ticker MSOL. However, no definitive launch dates have been announced, as these remain contingent on the SEC’s clearance. The market is closely watching these developments, as the approval of these products would further solidify the institutional adoption of cryptocurrencies as a legitimate asset class within traditional finance.

Fees Set Below Every Existing Competitor: A Race to the Bottom

The most striking disclosure in Thursday’s filings pertains to the fee structure. Both the Morgan Stanley Ethereum Trust and the Morgan Stanley Solana Trust are set to charge an annual sponsor fee of 0.14%. This fee will be calculated daily based on each fund’s net asset value and disbursed on a monthly basis.

This proposed fee is remarkably competitive, undercutting the current offerings of every existing ETH and SOL ETF on the market. As of recent data compiled by SoSoValue, Grayscale’s Mini Ethereum Trust currently holds the distinction of the lowest Ethereum ETF sponsor fee at 0.15%. In the Solana ETF arena, Franklin Templeton’s SOEZ leads with the lowest rate at 0.19%. Noteworthy industry analyst Eric Balchunas of Bloomberg commented on this development, stating that the 14 basis point rate would indeed make these Morgan Stanley funds "the cheapest in the U.S. and world."

The decision to apply this aggressive, ultra-low pricing strategy to both Ether and Solana suggests a clear intention by Morgan Stanley to compete primarily on cost. By leveraging its extensive wealth management and advisory network, the firm aims to channel client assets into its own products, thereby diverting them from competing offerings.

This fee strategy is a direct echo of the approach Morgan Stanley employed to penetrate the Bitcoin ETF market. The bank’s Bitcoin Trust (MSBT), which launched in April, also benefited from a competitive 0.14% sponsor fee, undercutting established spot Bitcoin funds at the time of its introduction. The success of this strategy is already evident, as MSBT had garnered $300.7 million in cumulative net inflows as of June 18, demonstrating institutional investor appetite for lower-cost digital asset exposure. This precedent suggests that Morgan Stanley is not only looking to enter the Ethereum and Solana ETF markets but to dominate them through price competitiveness.

Staking Baked Into Both Funds: Enhancing Yield Potential

Beyond the compelling fee structure, the amendments introduce a crucial feature: staking functionality for both the Ethereum and Solana ETFs. This capability is poised to provide Morgan Stanley’s ETFs with a significant yield advantage over funds that merely hold cryptocurrencies without actively participating in network validation.

Under the proposed structure, an impressive 95% of staking rewards will remain within the trusts. The remaining 5% will be allocated to staking service providers and custodians as compensation for their roles in managing the staking operations. The chosen staking service providers for both funds are Figment Inc., Galaxy Blockchain Infrastructure LLC, and Coinbase Canada, Inc., all reputable entities within the digital asset infrastructure space.

Importantly, the filing clarifies that the sponsor itself, Morgan Stanley, will not be entitled to any share of staking rewards beyond its management fee. This structure is designed to directly benefit investors, who stand to gain not only from potential price appreciation of ETH and SOL but also from the ongoing yield generated through staking. This integrated yield generation mechanism represents a significant differentiator in a market where most competing products primarily offer price exposure alone.

The inclusion of staking is particularly relevant for Ethereum, which transitioned to a proof-of-stake (PoS) consensus mechanism with "The Merge" in September 2022. Staking allows validators to earn rewards for securing the network and processing transactions. For Solana, which also operates on a PoS model, staking similarly incentivizes network participation and security. By offering a product that incorporates this yield-generating component, Morgan Stanley is tapping into a key feature of these underlying blockchain networks that appeals to yield-seeking investors.

Ethereum Staking: Disclosing Queue and Timing Risks

The Ethereum ETF filing delves into considerable operational detail regarding the mechanics of staking, including network-specific constraints that can impact the speed at which assets begin to generate rewards. As of May 18, 2026, approximately 3.64 million ETH were reportedly in the queue to be activated on validators. Ethereum’s network architecture imposes limitations on the number of validators that can enter the staking queue, capping it at 56 per epoch, which translates to roughly 57,600 ETH per day.

Based on these figures, Morgan Stanley has estimated that newly staked Ether could experience an activation delay of approximately 63 days before becoming eligible to earn staking rewards. This disclosure is crucial for setting investor expectations and highlights the operational realities of participating in Ethereum’s staking ecosystem.

Furthermore, the filing also addresses the "slashing risk." This is an inherent mechanism within proof-of-stake networks where staked assets can be penalized and removed from a validator’s account if network rules are violated or if a validator fails to perform its duties. While this is a standard disclosure for any fund structure that incorporates staking, its inclusion underscores Morgan Stanley’s commitment to transparency regarding the potential risks associated with managing staked assets.

Solana Mechanics Differ Slightly, Emphasizing Key Custody Separation

The Solana filing follows a broadly similar framework to the Ethereum amendment but incorporates a few key distinctions that reflect the specific architecture of the Solana network. Unlike the Ethereum filing, the Solana amendment does not disclose any daily staking capacity limits, suggesting a potentially more fluid activation process for new staked assets.

A significant operational difference highlighted in the Solana filing is Morgan Stanley’s statement that custodians involved in the staking process will not retain control over the private keys associated with delegated SOL assets. This deliberate design choice serves to maintain a separation between key custody functions and the staking operations, thereby mitigating a particular category of operational risk. By keeping these functions distinct, the potential for unauthorized access or misuse of private keys is reduced, enhancing the overall security posture of the fund.

Broader Crypto ETF Landscape and Morgan Stanley’s Strategic Positioning

Morgan Stanley’s aggressive move into the spot Ethereum and Solana ETF space occurs against a backdrop of a rapidly expanding and maturing cryptocurrency ETF market. The disclosures arrive as asset managers continue to collaborate with U.S. regulators to refine fund structures that effectively combine direct cryptocurrency exposure with the potential for staking-based yield generation. The SEC’s recent approval of BlackRock’s Bitcoin Premium Income ETF, which commenced trading on June 16, further signals the regulator’s increasing receptiveness to innovative crypto fund structures that offer more than just price tracking.

Morgan Stanley has also garnered considerable market attention regarding a potential XRP ETF filing. This speculation was fueled by the institution’s recent revelation of holdings in existing XRP ETFs, prompting widespread anticipation of a forthcoming application. If approved, the proposed ETH and SOL products, alongside a potential XRP ETF, would extend the bank’s presence across all three of the largest digital assets currently available via U.S. spot ETFs. This comprehensive offering would position Morgan Stanley as a central player catering to diverse institutional investor needs in the digital asset space.

The amended filings represent a critical checkpoint in the regulatory approval process. By proposing the lowest fees in both the Ethereum and Solana ETF markets, incorporating a built-in staking yield component from inception, and building on the demonstrated success of its Bitcoin ETF in attracting institutional capital, Morgan Stanley is strategically positioning itself as a serious, long-term contender in the crypto ETF arena. This is not merely an opportunistic late entry but a calculated move to establish market leadership through competitive pricing and innovative product design, potentially reshaping the competitive dynamics of the entire digital asset ETF industry. The firm’s commitment to these products suggests a belief in the sustained growth and institutionalization of cryptocurrencies.