The global banking landscape is approaching a pivotal juncture that could fundamentally alter the relationship between traditional financial institutions and the world’s largest cryptocurrency. Market analysts and industry stakeholders are closely monitoring the upcoming 2026 updates to the Basel III framework, the international regulatory accord that sets capital requirements for banks. According to prominent market analyst Nic Puckrin and other financial experts, a potential downward revision of the risk rating for Bitcoin (BTC) could serve as the catalyst for a "huge" influx of liquidity, finally allowing the primary engines of the global economy to integrate digital assets into their balance sheets.

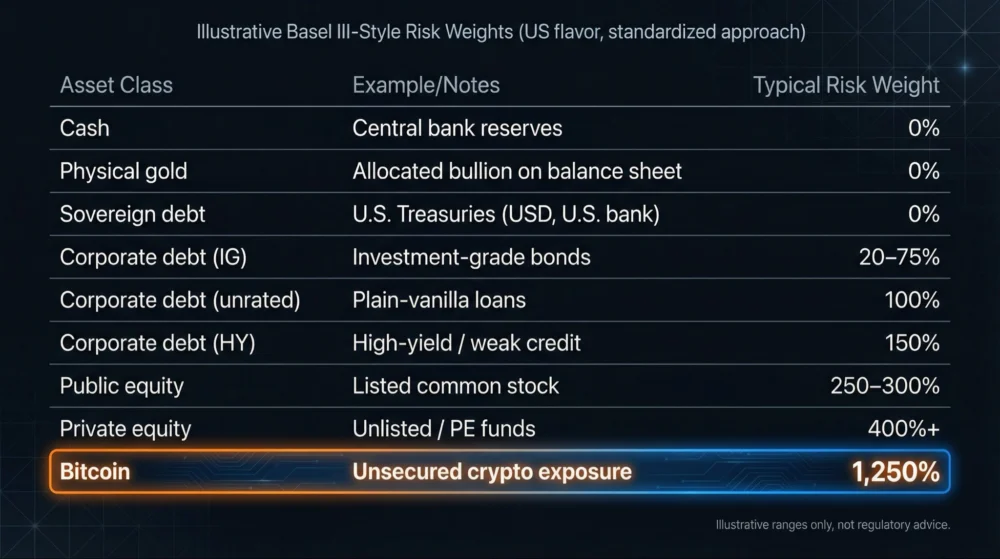

Under the current standards established by the Basel Committee on Banking Supervision (BCBS), Bitcoin and other unbacked digital assets are categorized in the highest possible risk tier. This classification carries a 1,250% risk weight, a figure that effectively mandates a dollar-for-dollar capital reserve. In practical terms, for every $1 worth of Bitcoin a bank holds, it must maintain $1 of Tier 1 capital as a buffer. This 1:1 ratio is designed to be intentionally prohibitive, making it economically unfeasible for regulated banks to provide custody, trading, or treasury services involving Bitcoin.

The debate over these requirements has intensified following a recent announcement from the United States Federal Reserve. The Fed has introduced a proposal detailing the domestic implementation of these international rules, opening a 90-day window for public comment. This period is viewed by many in the crypto-financial sector as a critical opportunity to lobby for more nuanced risk weights that reflect the maturing liquidity and institutional adoption of Bitcoin.

The Mechanics of Risk Weighting and Capital Adequacy

To understand the magnitude of the 1,250% risk weight, one must compare it to the treatment of traditional financial instruments. Risk weighting is the mechanism regulators use to determine how much capital a bank must hold to protect against potential losses. Lower-risk assets require less capital, allowing banks to use their liquidity more efficiently for lending and investment.

According to Jeff Walton, the Chief Risk Officer at Bitcoin treasury firm Strive, the current disparity between Bitcoin and other asset classes is stark. Under the existing Basel III framework, investment-grade corporate bonds typically carry a risk weight of approximately 75%. Even more conservative assets, such as physical cash, gold, and sovereign government bonds (like US Treasuries), are assigned a 0% risk weight. This 0% rating implies that regulators view these assets as essentially "risk-free" in terms of capital erosion, allowing banks to hold them without setting aside additional reserve capital.

Walton argues that the current 1,250% weighting for Bitcoin suggests a fundamental mispricing of risk by global regulators. While Bitcoin remains volatile compared to the US dollar, its liquidity profile and decade-long survival record have led many to argue that it should be treated more like a volatile commodity or an emerging equity, rather than a "toxic" asset requiring a 100% capital backup.

Chronology of Basel’s Crypto Regulatory Evolution

The path toward the 2026 implementation began in the wake of the 2008 financial crisis, which necessitated the original Basel III reforms to ensure banks held enough high-quality liquid assets. However, the specific focus on digital assets is a more recent development:

- June 2021: The BCBS released its first consultative document on the prudential treatment of crypto-asset exposures. This document introduced the concept of "Group 1" assets (tokenized traditional assets and stablecoins with effective stabilization mechanisms) and "Group 2" assets (unbacked crypto-assets like Bitcoin).

- December 2022: The Committee finalized its standard for bank exposures to crypto-assets. It confirmed the 1,250% risk weight for Group 2 assets and set an exposure limit, stating that a bank’s total exposure to Group 2 crypto-assets should generally not exceed 1% of its Tier 1 capital.

- February 2024: A coalition of crypto treasury executives and advocacy groups began a coordinated push for reform. They argued that the 1,250% weight prevents banks from participating in the "blockchain economy" and deprives the market of the stability that institutional custodians provide.

- Mid-2024: The US Federal Reserve, alongside the FDIC and the OCC, began formalizing the "Basel III Endgame" in the United States. This included the current 90-day public comment window regarding the implementation of these standards.

- January 1, 2026: The scheduled date for the new Basel standards to take full effect globally.

The "Chokepoint" Narrative: Subtle Regulatory Suppression

The restrictive nature of the Basel rules has led some industry leaders to describe them as a sophisticated form of "de-banking." Chris Perkins, President of the investment firm CoinFund, suggests that these capital requirements represent a "covert" form of industry suppression. While high-profile enforcement actions or the "Operation Chokepoint 2.0" narrative focus on the direct closure of bank accounts for crypto firms, the Basel rules act on a structural level.

"It’s a very nuanced way of suppressing activity by making it so expensive for the bank to do those activities," Perkins noted. By setting the capital cost so high, regulators ensure that even if a bank wants to offer Bitcoin services, the return on equity (ROE) for that business line would be negative or uncompetitive. This effectively keeps the traditional banking sector and the digital asset sector bifurcated, preventing the "bridge" that many institutional investors have been seeking.

Potential Implications of a Risk Weight Reduction

If the public comment window and subsequent negotiations lead to even a marginal reduction in Bitcoin’s risk weight—for instance, to 250% or 500%—the economic calculus for global banks would change overnight.

A lower risk weight would mean that banks could hold Bitcoin on their balance sheets while only needing to back a fraction of the value with reserve capital. This would likely lead to several key developments:

Increased Institutional Custody

Currently, most Bitcoin is held by specialized digital asset custodians or through ETF structures. If capital rules are relaxed, "G-SIBs" (Global Systemically Important Banks) like JPMorgan Chase, Goldman Sachs, or BNY Mellon could more easily offer direct custody. This would provide a level of security and insurance that could attract trillions of dollars in conservative institutional capital that is currently sidelined.

Integration into Treasury Management

Corporations often look to their banking partners for treasury management advice. If banks can hold Bitcoin, they can more easily facilitate corporate treasury allocations into the asset, similar to how they handle gold or foreign exchange reserves.

Enhanced Market Liquidity and Stability

The entry of large-scale bank liquidity would likely dampen Bitcoin’s notorious volatility over the long term. Banks act as market makers and providers of deep liquidity; their participation would professionalize the market structure and potentially reduce the "Sats-to-USD" spreads in large-scale transactions.

Official Responses and the Road to 2026

The Federal Reserve’s move to open a comment window suggests that the US regulatory body is at least willing to hear the industry’s concerns regarding "gold-plating"—the practice of making domestic rules even stricter than international standards. Financial advocacy groups, including the Bitcoin Policy Institute and various crypto-focused PACs, are expected to submit extensive data during this window to prove that Bitcoin’s liquidity profile warrants a more favorable risk classification.

However, resistance remains. Proponents of the strict 1,250% rule argue that the crypto market’s history of contagion—most notably the 2022 collapses of Celsius, Voyager, and FTX—justifies a "better safe than sorry" approach. They maintain that the primary goal of Basel III is to protect the taxpayer-funded safety net of the banking system from the high-velocity risks associated with unbacked digital assets.

Strategic Analysis: A New Era for Digital Finance?

The outcome of the Basel III revisions will likely dictate the trajectory of Bitcoin’s institutional adoption for the remainder of the decade. If the rules remain unchanged, Bitcoin will likely continue to grow as an "outside" asset, facilitated primarily by non-bank financial institutions and ETFs. While this has been successful thus far, it limits the asset’s utility within the broader plumbing of the global financial system.

Conversely, if the 2026 rules provide a pathway for banks to hold Bitcoin with a risk weight comparable to other volatile equities or commodities, it would signal the end of the "experiment" phase for Bitcoin and its graduation into a permanent fixture of global finance. As Nic Puckrin suggested, the "door is opening," but the final width of that opening depends on the technical negotiations currently taking place in Washington and Basel.

As the 90-day comment period progresses, the industry will be looking for signals from the Fed and other central banks. Any hint of a shift toward a more accommodating stance could be a major bullish signal for the market, preempting the actual implementation in 2026. For now, the crypto industry remains in a state of watchful anticipation, recognizing that the "Basel III Endgame" may well be the beginning of Bitcoin’s full institutional integration.