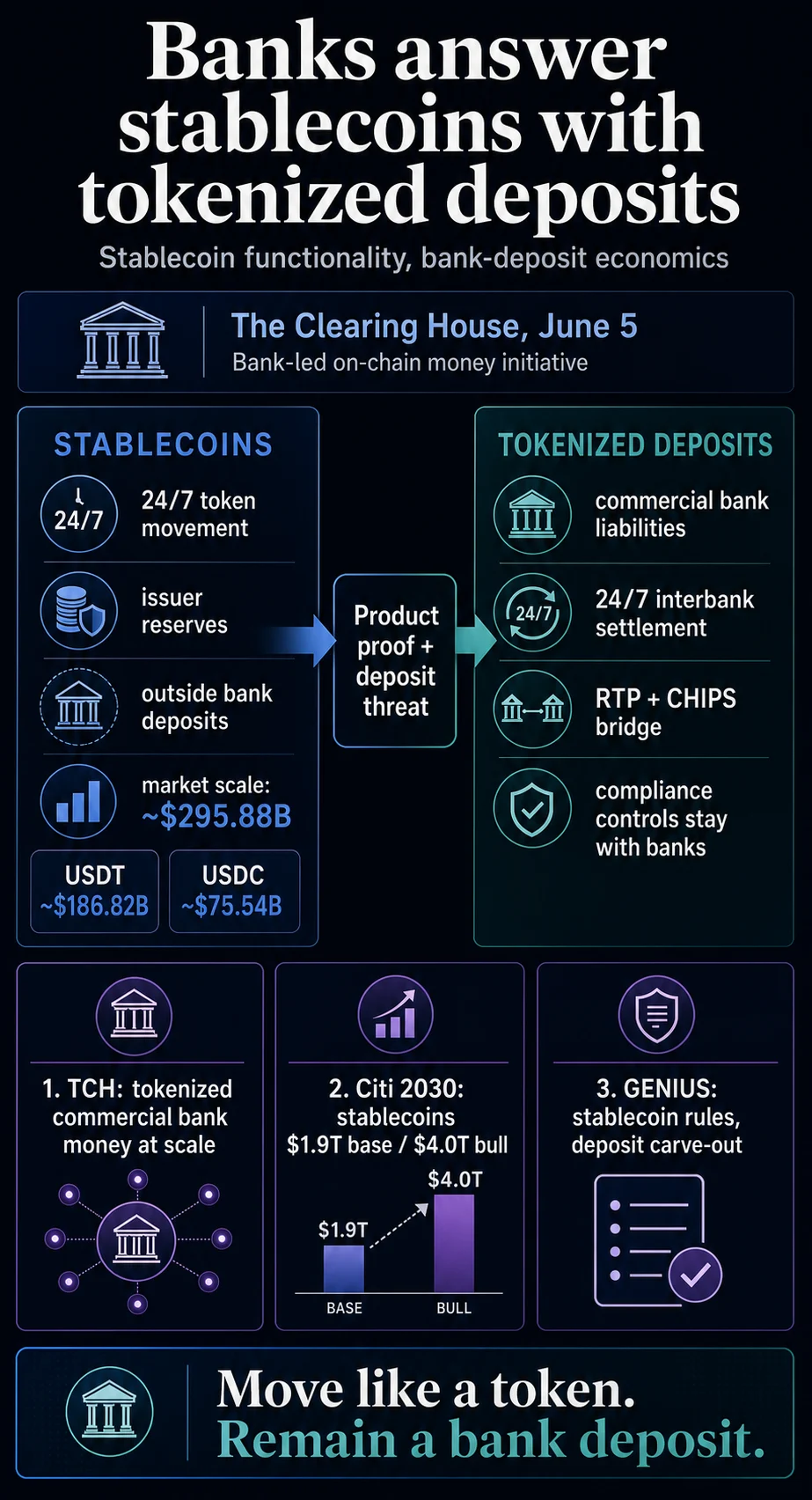

The Clearing House (TCH), the influential bank-owned operator of core U.S. payment infrastructure, has announced a groundbreaking initiative to enable banks to settle deposits directly on-chain, a move that could fundamentally reshape the digital dollar landscape and challenge the ascendancy of stablecoins. This strategic announcement on June 5th signifies a unified response from the largest U.S. banks to the growing demand for round-the-clock, blockchain-enabled payment capabilities, while crucially aiming to retain control over customer balances, compliance frameworks, and the lucrative economics of traditional deposit systems.

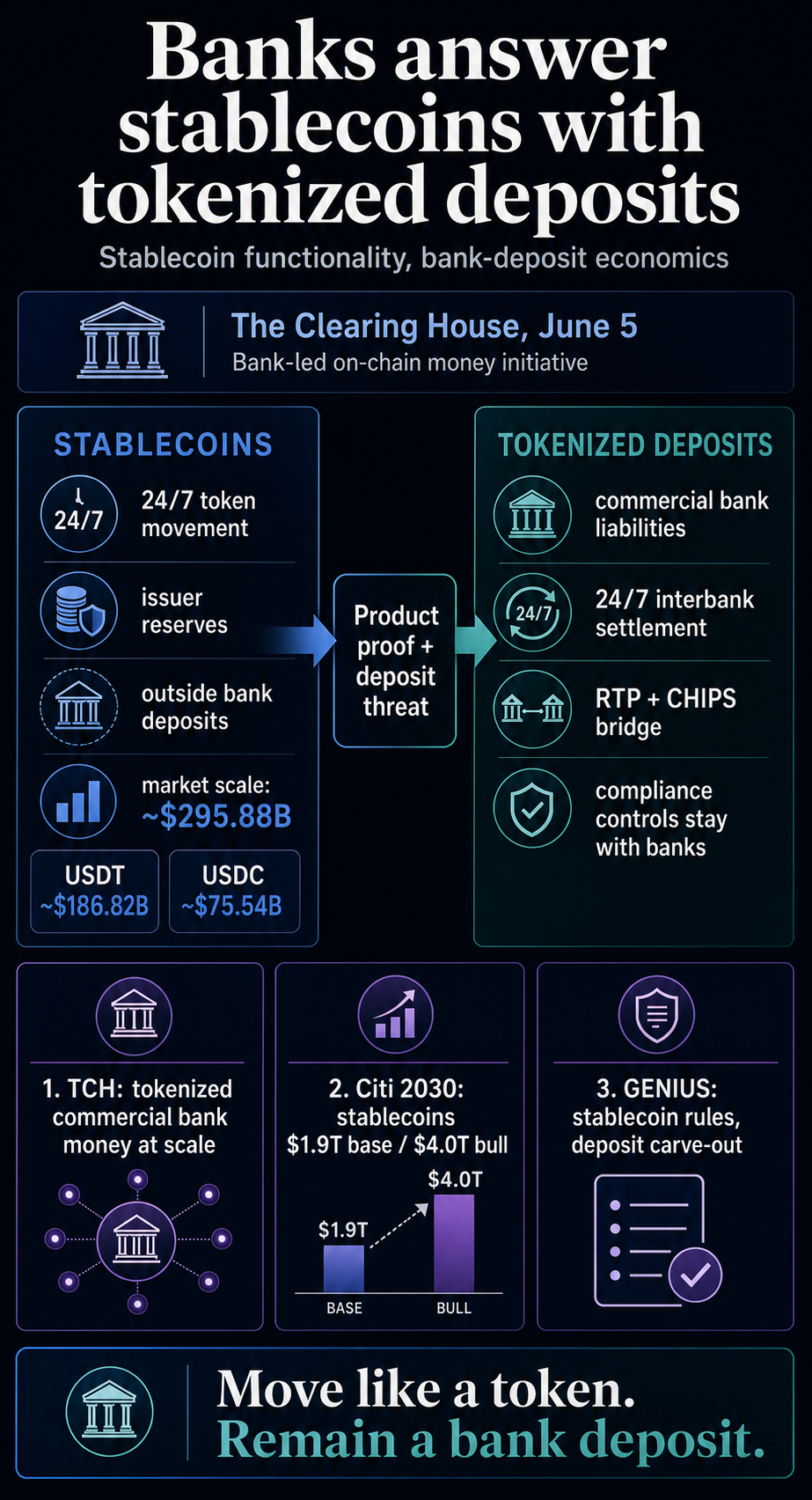

The proposed system is designed to facilitate the clearing and settlement of tokenized commercial bank money at scale. According to The Clearing House’s official announcement, this initiative will support 24/7 on-chain clearing and settlement of tokenized deposits between financial institutions. Crucially, it will also bridge blockchain-based activities with established fiat payment rails such as RTP (Real-Time Payments) and CHIPS (Clearing House Interbank Payments System), creating a hybrid infrastructure that leverages the strengths of both traditional and distributed ledger technologies.

This strategic architecture offers banks a distinct alternative to bank-issued stablecoins. While stablecoins facilitate the movement of dollar claims outside the traditional deposit system, tokenized deposits aim to replicate the digital features of these assets while keeping the underlying funds firmly within the regulated banking system as commercial bank liabilities. This approach can be viewed as both a defensive maneuver to protect the existing banking ecosystem and an opportunistic embrace of technological innovation driven by market demand. Banks are increasingly recognizing the appeal of crypto rails, particularly as stablecoins have demonstrated a clear appetite for tokenized dollars, and simultaneously pose a potential threat to the deposit base that underpins banking profitability.

Bank Money Embraces Crypto Rails: A Strategic Pivot

The Clearing House’s entry into this burgeoning market is underpinned by its unique position as a payments infrastructure provider owned by the very institutions it serves. Its ownership page proudly states it is owned by the world’s largest commercial banks, with the recent announcement specifying that 25 of the nation’s largest financial institutions are stakeholders. This collective ownership is paramount, as the proposed network intends to keep bank money within bank-controlled rails while providing deposits with a settlement layer akin to digital assets.

The announcement details tokenized deposits capable of settling between banks, carrying richer transactional data, and supporting automated workflows. The integration with existing systems like RTP and CHIPS is a critical component, establishing a controlled conduit between on-chain activities and established bank payment systems. This is not entirely uncharted territory for The Clearing House; the organization already possesses a precedent for tokenization within bank-controlled payment flows through its DDA Token Service. This service replaces sensitive customer account numbers with tokens, managing the secure translation back to account numbers, thereby preserving compliance visibility. This existing Open Banking payment-token product demonstrates the operational principle banks are keen to extend: minimizing the exposure of sensitive bank information, maintaining robust compliance oversight, and ensuring the bank remains the central point of control.

The Economic Imperative: Why Banks Are Investing in Tokenized Deposits

Research from financial giants like Citi underscores the urgent need for banks to address the evolving digital dollar landscape. Citi’s "Stablecoins 2030" report projected a significant surge in stablecoin issuance, forecasting up to $1.9 trillion in its base case and $4.0 trillion in its bull case by 2030. The same report also posits that stablecoins will coexist with bank-issued tokens, such as tokenized deposits, and that the transaction volumes for bank tokens could ultimately surpass those of stablecoins by the end of the decade.

Furthermore, separate research from Citi, titled "Tokenization 2030," highlights the institutional drivers behind this shift. Current stablecoin models can introduce fragmentation and pre-funding challenges for institutional settlement processes. Tokenized deposits, issued by regulated banks, are emerging as a key alternative for market participants seeking on-chain liquidity solutions.

The fundamental differences between tokenized deposits and payment stablecoins are critical to understanding the strategic intentions of banks:

| Question | Tokenized Deposits | Payment Stablecoins |

|---|---|---|

| Who stands behind the money? | A regulated bank deposit liability. | A permitted or foreign stablecoin issuer backed by reserves. |

| Banks’ answer to stablecoins? | 24/7 settlement, programmability, interoperability, and richer data within bank rails. | On-chain transferability, global availability, and token-based settlement. |

| How does yield fit? | Deposit economics remain with banks and their account relationships. | Issuer-paid interest or yield solely for holding, using, or retaining the payment stablecoin. |

| Strategic incentive? | Keep customer money and compliance within the bank system. | Expand digital-dollar usage through non-deposit tokens and reserve-backed payment assets. |

This clear delineation of responsibilities and economic models is central to The Clearing House’s strategy.

Navigating the Regulatory Maze: Preserving the Legal Distinction

The policy environment surrounding digital assets plays a significant role in explaining why banks are opting for tokenized deposits rather than directly issuing stablecoins. The recently enacted GENIUS Act provides a regulatory framework for payment stablecoins. It mandates that permitted issuers maintain reserves of at least one-to-one and prohibits issuer-paid interest or yield solely for holding, using, or retaining a payment stablecoin. Crucially, the legislation explicitly excludes deposits recorded using distributed ledger technology from the definition of a payment stablecoin.

This exclusion is a cornerstone of the banks’ strategic advantage. It allows deposits to be recorded and transacted in novel ways without being classified as payment stablecoins. The legal classification is paramount, as it determines whether the money is treated as a traditional bank deposit or as a tokenized claim on a stablecoin issuer’s reserves.

The FDIC has reinforced this distinction. In its April 2026 proposed rule summary, the FDIC clarified that deposits held as reserves backing a payment stablecoin would not receive pass-through insurance coverage for stablecoin holders. Furthermore, the FDIC stated that the deposit insurance treatment for deposits is independent of whether an insured depository institution records those deposit liabilities using distributed ledger technology. Although this rule is still in its proposed stage, its direction is clear: tokenized deposits empower banks to argue that customers can access blockchain-style settlement mechanisms without departing from established deposit law.

In contrast, stablecoins, while offering a dollar token, provide holders with a different claim and insurance profile compared to ordinary bank deposits. The Office of the Comptroller of the Currency (OCC) is also actively developing regulations to implement the GENIUS Act, focusing on permitted payment stablecoin issuers, foreign issuers, and related custody activities. This regulatory scaffolding around stablecoins is precisely what the banks’ tokenized-deposit initiative is designed to navigate. The Clearing House network, therefore, positions itself within the tokenized-deposit category rather than venturing into the realm of stablecoin issuance. The product aims to replicate the efficient settlement experience that has made stablecoins popular, but with the intent of maintaining legal claims, balance-sheet treatment, and compliance frameworks firmly within the traditional banking system.

The critical question that remains is whether this carefully controlled bank-led version can ultimately match the speed, accessibility, and reach that users have come to expect from dollar tokens in the broader digital asset ecosystem.

The Underlying Battle: Deposit Economics and Market Capture

At its core, The Clearing House’s initiative represents a strategic response by banks to the market signals generated by stablecoins. The sheer scale of the stablecoin market makes it an unavoidable concern for traditional financial institutions. As of June 8th, data indicated a stablecoin sector market capitalization of approximately $296 billion, with major players like Tether (USDT) accounting for roughly $187 billion and USD Coin (USDC) at around $76 billion. The broader cryptocurrency market, valued near $2.2 trillion, further emphasizes that stablecoins are no longer a niche product but a significant component of the digital asset landscape.

This growth has inevitably ignited policy debates. The tension between bank-run warnings, the defense of tokenized deposits, pressures from banks regarding stablecoin yields, and the fundamental question of who captures the economics of the digital dollar are all intertwined. The CLARITY Act, which has advanced through the House, adds another layer by establishing market structure rules for digital assets, even as the debate over payment rails, wallets, reserves, and yields continues concurrently.

Banking groups have been vocal about their apprehensions. The American Bankers Association, joined by 52 state banking associations, cautioned Congress that stablecoin incentives mimicking yield could disintermediate traditional deposit-taking and lending activities. Their concern is straightforward: if customers can hold dollar tokens that offer faster transactions and attractive yields, a portion of their balances might migrate away from conventional bank accounts.

However, the magnitude of this risk is a subject of ongoing analysis. The Council of Economic Advisers modeled the potential baseline lending impact of prohibiting stablecoin yield, estimating it at $2.1 billion, with a worst-case scenario suggesting an additional $531 billion in aggregate lending. These are model outputs, not yet observed deposit flight.

The Federal Reserve’s December analysis offers a more nuanced perspective. It suggests that the impact of stablecoins on bank deposits is contingent on various factors, including the source of demand, how issuers invest their reserves, and whether issuers gain access to central bank accounts. The Fed noted that stablecoins could reduce deposits, recycle deposits into different forms, or alter the structure of bank funding even if the total volume of deposits remains stable.

This complex interplay of market forces, regulatory developments, and economic considerations highlights why The Clearing House’s move is simultaneously defensive and offensive. It aims to safeguard existing deposit relationships while strategically incorporating the elements of the stablecoin product that have proven popular with customers and institutions. The promise of faster settlement, programmable money movement, and enhanced connectivity to digital asset markets has become a critical factor in the evolving landscape of banking products.

The unresolved challenge lies in determining whether a bank-led, controlled network can successfully replicate the open-network advantages that initially propelled stablecoins to prominence. The Clearing House’s announcement leaves key details regarding launch timing, ledger design, operating rules, and public-chain interoperability yet to be finalized.

For the present, the observable trends strongly support a more direct conclusion than either side’s rhetoric might suggest. Stablecoins have acted as a catalyst, compelling banks to innovate. Tokenized deposits represent the banks’ response: enabling money to move with token-like efficiency, but crucially, keeping that money firmly within the established banking system.