The Australian Securities and Investments Commission (ASIC) has issued a formal warning to young investors regarding the growing reliance on social media influencers and generative artificial intelligence for financial guidance. According to a comprehensive study released by the regulator on Sunday, a significant portion of "Generation Z"—defined in this context as individuals aged 18 to 28—is making high-stakes financial decisions based on information from unverified and often unlicensed digital sources. The study, conducted through ASIC’s "Moneysmart" program, highlights a precarious trend where one in four Gen Z Australians now holds cryptocurrency, often influenced by "finfluencers" whose primary objective is platform engagement rather than the provision of accurate, regulated financial advice.

ASIC Commissioner Alan Kirkland emphasized that while the younger demographic displays a commendable appetite for financial literacy and investment, the sources they frequent are frequently unreliable. The regulator’s findings suggest that the quest for financial independence is leading many young Australians into high-risk territories, including volatile crypto markets and complex superannuation maneuvers, without the safety net of professional oversight. The report underscores a critical disconnect: Gen Z investors desire trustworthy content but struggle to distinguish between a genuine financial recommendation and a marketing tactic designed to go viral.

A Chronology of Regulatory Vigilance and Digital Shifts

The current warning is the latest development in a multi-year effort by ASIC to police the digital frontier of financial services. To understand the gravity of the current situation, it is necessary to examine the timeline of ASIC’s interventions and the evolving habits of Australian retail investors.

In June 2023, ASIC initiated a significant crackdown on the "finfluencer" phenomenon. During this period, the regulator issued warning notices to 18 prominent social media personalities suspected of promoting high-risk financial products and providing unlicensed advice. This move followed a 2022 information sheet (INFO 225) which clarified that influencers could face up to five years in prison if they provide financial services without a license.

Between November 28 and December 10, 2023, ASIC conducted the survey that serves as the foundation for its current advisory. The study polled 1,127 respondents aged 18 to 28, seeking to map the digital landscape of financial decision-making. By early 2024, the data revealed a stark reality: the traditional financial advisor was being replaced by the TikTok algorithm and the AI chatbot.

In late January 2024, ASIC further signaled its intent by announcing that its top priorities for the 2026 fiscal year would include targeting firms—particularly in the crypto and AI sectors—that exploit licensing "gray areas" in the Australian payments and investment landscape. The release of the full "Moneysmart" Gen Z study in March 2024 represents the culmination of this research phase, providing the regulator with the empirical evidence needed to justify stricter enforcement of digital advice.

Analyzing the Data: The Trust Paradox

The statistical breakdown of the ASIC study reveals a "trust paradox" among young investors. While Gen Z is often characterized as being digitally savvy and skeptical of traditional institutions, they exhibit surprisingly high levels of trust in unregulated digital entities.

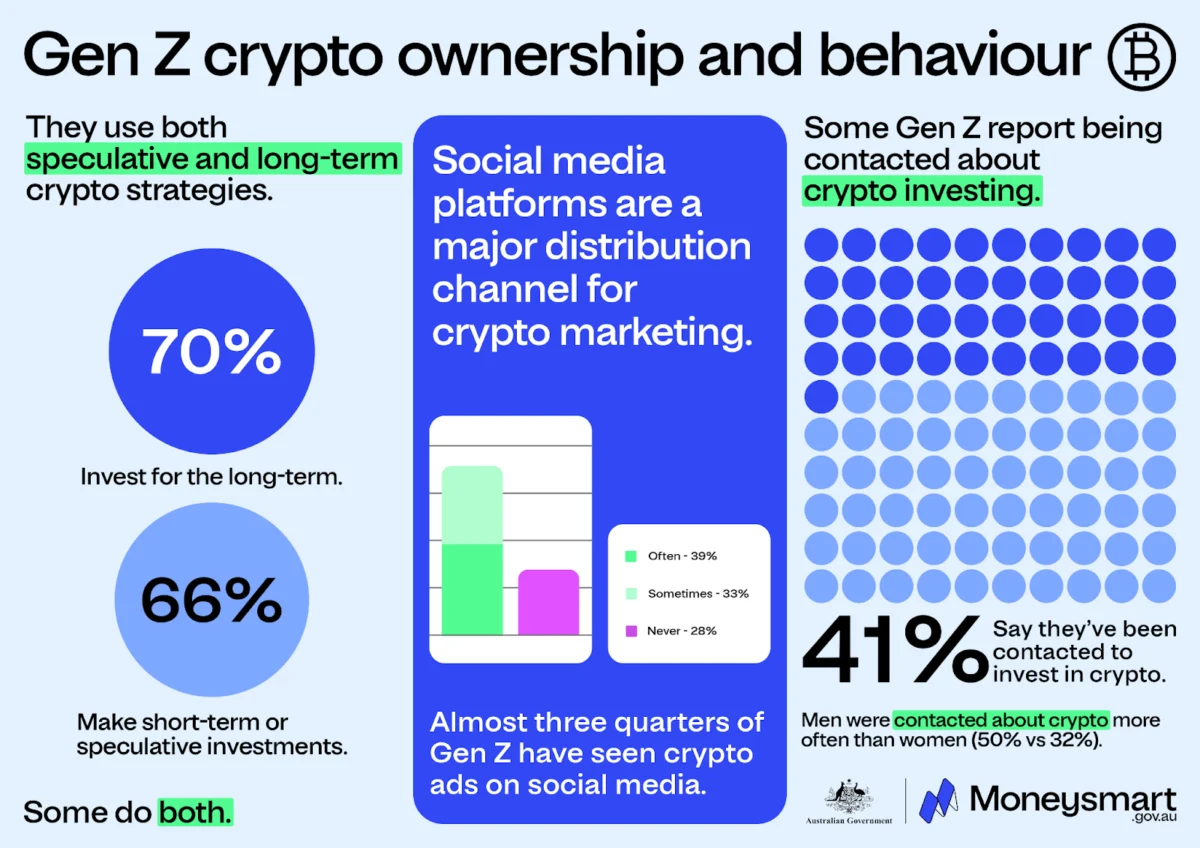

The survey found that 63% of Gen Z Australians utilize social media platforms as their primary source for financial information and guidance. Within this group, YouTube remains a dominant force, with 30% of respondents citing it as a go-to platform for investment education. Furthermore, 56% of respondents admitted they "somewhat or completely trust" financial information found on social media, while 52% expressed the same level of confidence in "finfluencers."

Perhaps most striking is the role of Artificial Intelligence. Despite AI being a relatively new tool in the public consciousness, it emerged as the most trusted source among the "Zoomer" demographic, with 64% of respondents indicating they trust financial information derived from AI platforms. This trust exists despite well-documented issues with AI "hallucinations"—where chatbots present false information as fact—and the lack of accountability when an AI-driven trade results in financial loss.

Regarding asset allocation, the study confirmed that cryptocurrency has become a mainstream asset for the youth. Twenty-three percent of Gen Z Australians now own crypto assets. However, the motivation for these purchases is often driven by external digital pressure; 29% of crypto holders in this age group admitted to trading based specifically on social media and influencer content.

Official Responses and Regulatory Concerns

ASIC Commissioner Alan Kirkland, speaking with the Australian Financial Review (AFR), articulated the regulator’s specific concerns regarding the marketing tactics used to lure young investors. Kirkland noted that the volatility of the crypto market is often exacerbated by global forces that are nearly impossible for a retail investor in Australia to predict or understand.

"We’re conscious that there’s a lot of marketing activity on social media to encourage crypto investment, and our work has shown some that is actually encouraging people to invest in scams," Kirkland stated. He warned that influencers often set "unrealistic expectations" regarding market returns, failing to mention the intricacies of long-term risk management.

A particularly sensitive area for the regulator is the $4.5 trillion Australian superannuation market. Superannuation, the mandatory retirement savings system in Australia, is often an individual’s largest financial asset. Kirkland flagged that unqualified influencers are increasingly targeting this sector, encouraging young people to switch their superannuation funds into riskier, often inappropriate, investment vehicles.

"We see it most where people are lured in through social media ads and then encouraged to switch their super," Kirkland said. "That’s why disreputable people often target it and why it can be so tragic if people are encouraged to put it into a risky investment."

The Legal Threshold for AI and Digital Advice

One of the most significant takeaways from ASIC’s recent communication is the clarification of how Australian law applies to AI-generated financial advice. The regulator has put the industry on notice: if an AI tool provides a recommendation that takes into account an individual’s personal circumstances, it constitutes "personal advice."

Under the Corporations Act 2001, any entity providing personal financial advice must hold an Australian Financial Services (AFS) license. This applies regardless of whether the advice is delivered by a human advisor or a large language model. ASIC is currently monitoring the integration of AI bots into services provided by various crypto exchanges, including MEXC, KuCoin, and Bitget, which have begun offering AI-powered "trading partners."

Kirkland’s warning serves as a preemptive strike against the automation of unlicensed advice. The regulator is "watching very closely" to see if these AI tools cross the line from general information to concrete financial recommendations. If an AI platform suggests a specific financial product to a user based on their data, the provider of that platform could be held liable for operating without a license.

Broader Implications for the Financial Industry

The shift in Gen Z’s behavior has profound implications for the future of the Australian financial services industry. The traditional model of financial advice—often characterized by face-to-face meetings and high entry costs—is being disrupted by the "engagement economy."

-

The Erosion of Fiduciary Standards: Unlike registered financial advisors, who have a legal fiduciary duty to act in their clients’ best interests, social media influencers are often incentivized by affiliate links, sponsorships, and view counts. This creates a fundamental conflict of interest that young investors may not fully grasp.

-

The Gamification of Investing: The reliance on social media and AI often leads to the gamification of finance. When investment decisions are made based on 60-second viral clips or quick chatbot prompts, the gravity of potential loss is often diminished. This can lead to "revenge trading" or excessive risk-taking during market downturns.

-

Regulatory Evolution: ASIC’s focus on the "digital perimeter" indicates a shift in regulatory strategy. Instead of just monitoring traditional banks and brokerages, the regulator must now develop sophisticated tools to monitor decentralized social media platforms and evolving AI algorithms.

-

The Need for Digital Literacy: The "Moneysmart" study suggests that while young people are "online," they are not necessarily "financially literate" in a digital context. There is an urgent need for educational programs that teach investors how to verify the credentials of an online source and how to spot the hallmarks of a financial scam.

Conclusion: A Call for Caution in the Digital Age

As Australia moves toward 2026, ASIC’s stance is clear: the democratization of financial information through social media and AI is a double-edged sword. While it provides access to markets that were once the exclusive domain of the wealthy, it also opens the door to unprecedented levels of risk and fraud.

The regulator’s message to Gen Z is one of "sense-checking." Before acting on a tip from a YouTube video or an AI prompt, investors are urged to check the ASIC professional register to see if the source is licensed. In an era where a viral post can move markets and an AI can draft a portfolio in seconds, the fundamental principles of investing—due diligence, risk assessment, and regulatory compliance—remain more relevant than ever. The tragedy of a lost retirement fund or a wiped-out crypto wallet is a high price to pay for following the latest digital trend.