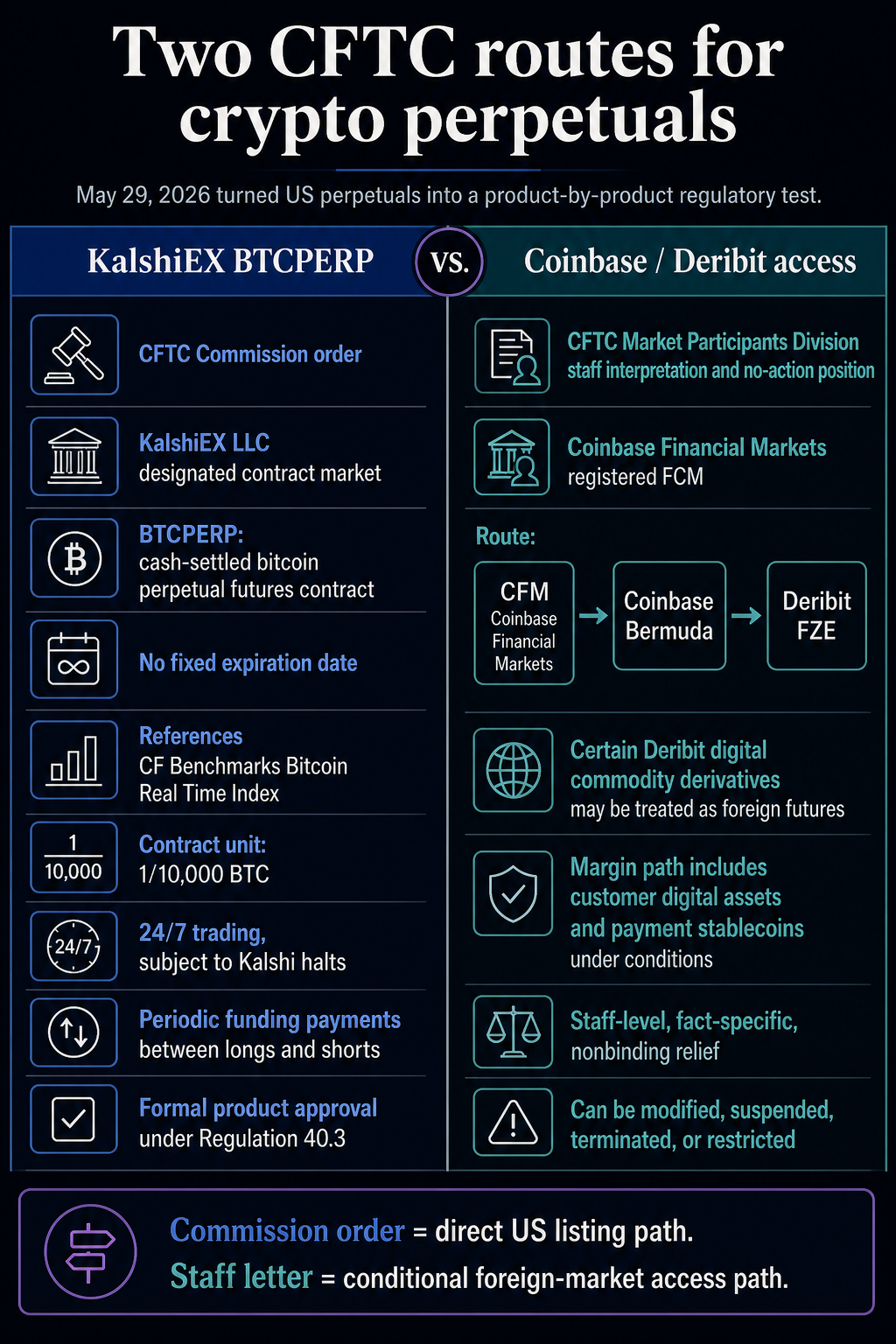

In a landmark shift for the United States digital asset landscape, the Commodity Futures Trading Commission (CFTC) has officially transitioned Bitcoin perpetual futures from the realm of offshore speculation into a regulated domestic framework. Through two distinct regulatory actions, the Commission has approved KalshiEX LLC to list a native Bitcoin perpetual contract (BTCPERP) and provided staff-level relief to Coinbase Financial Markets (CFM), allowing the latter to facilitate U.S. customer access to specialized derivatives products on the Deribit exchange. These moves collectively represent a fundamental change in how the U.S. government views crypto-native instruments, moving beyond traditional expiring futures toward the most liquid segment of the global cryptocurrency market.

The significance of these approvals cannot be overstated. Perpetual futures, or "perps," have long been the primary engine of crypto market volatility and liquidity, accounting for an estimated 80% of total global trading volume. Unlike traditional futures, which have a set expiration date and require traders to "roll" their positions into new contracts, perpetuals have no expiry. This structure allows traders to maintain long-term directional exposure with high leverage, but it has historically been confined to offshore, non-U.S. regulated platforms due to the complexities of fitting the product into the Commodity Exchange Act (CEA).

The Dual-Path Regulatory Framework

The CFTC’s actions on May 29, 2026, established two separate but parallel routes for onshoring crypto derivatives. The first route, granted to KalshiEX LLC, is a formal Commission Order. Under Section 5c(c)(4) of the CEA and Commission Regulation 40.3, the CFTC approved Kalshi’s BTCPERP as a designated contract. This allows Kalshi, a registered Designated Contract Market (DCM), to list a cash-settled Bitcoin perpetual tied directly to the spot price of Bitcoin. Because this is a formal Commission Order, it carries significant legal weight and serves as a direct precedent for how perpetual contracts can be structured within the U.S.

The second route involves Coinbase Financial Markets. In this instance, the CFTC’s Market Participants Division issued a technical interpretation and a "no-action" position. This allows Coinbase, acting as a registered Futures Commission Merchant (FCM), to route U.S. customer orders for certain digital commodity derivatives to Deribit FZE, an affiliated foreign board of trade. While this staff-level relief is more conditional and fact-specific than the Kalshi order, it provides an immediate bridge for U.S. institutional and retail capital to reach the deep liquidity pools of the global derivatives market.

Technical Specifications of the BTCPERP Contract

The Kalshi approval provides a detailed blueprint for how a "true" perpetual can function under U.S. oversight. According to the CFTC order, the BTCPERP contract references the U.S. dollar spot price of one Bitcoin as measured by the CF Benchmarks Bitcoin Real Time Index. To ensure the contract price remains tethered to the actual spot market without a fixed expiration date, Kalshi utilizes a periodic funding payment mechanism.

In this model, funding payments are exchanged between long and short position holders. If the perpetual contract is trading at a premium relative to the spot price, long holders pay shorts; if the contract trades at a discount, short holders pay longs. This economic incentive forces the market price toward the underlying index price. The CFTC’s approval noted that Bitcoin’s unique market structure—specifically its 24/7 trading availability and deep, continuous spot liquidity—makes it uniquely suited for this perpetual structure. The agency clarified that this analysis is currently limited to Bitcoin and other digital commodities with similar market depth, explicitly excluding less liquid asset classes from this specific regulatory treatment.

A Chronology of the Onshoring Effort

The path to these approvals has been a multi-year process involving rigorous industry consultation and internal agency debate.

- April 2025: The CFTC issued a formal Request for Comment (RFC) regarding perpetual derivatives. The agency sought data on the risks of high leverage, the mechanics of automated liquidations, and the impact of 24/7 trading on market integrity.

- July 2025: Coinbase finalized its acquisition of a stake in Deribit, signaling a clear intent to integrate global derivatives liquidity into its U.S. operations.

- May 2026: Bitnomial received certification for products labeled as perpetual futures, though these carried different structural nuances than the "true" no-expiry model.

- May 28-29, 2026: Kalshi submitted its final BTCPERP proposal, which received rapid Commission-level approval, coinciding with the Coinbase staff-level relief.

This timeline illustrates a deliberate move by the CFTC to modernize the U.S. derivatives plumbing. By acknowledging that crypto markets operate 24/7, the agency is attempting to reduce the "weekend gap" risk that often plagues traditional CME Bitcoin futures, which close during non-business hours while the underlying spot market continues to trade.

Industry Reactions and Strategic Implications

The response from major industry players suggests that these approvals are viewed as a "unlock" for massive amounts of sidelined capital. Brian Armstrong, CEO of Coinbase, highlighted the disparity between domestic and international markets, noting that U.S. users have historically been "locked out" of approximately 80% of the global crypto market volume. By providing a regulated bridge to Deribit, Coinbase aims to capture a significant portion of the institutional flow that previously had to navigate complex offshore entities.

Michael Saylor, Executive Chairman of MicroStrategy, linked the guidance to the broader institutional adoption of Bitcoin. He suggested that the availability of regulated perpetuals and options provides a more robust framework for Bitcoin-backed credit strategies and corporate treasury management. For companies like MicroStrategy, the ability to hedge or gain exposure through CFTC-regulated instruments reduces the counterparty risk associated with offshore exchanges.

Chairman Mike Selig of the CFTC cast the Kalshi order as a fulfillment of a pledge to onshore crypto asset perpetuals. He emphasized that the goal is not just to allow these products, but to ensure they exist within a framework that includes federal oversight, customer protection, and market surveillance.

Comparing the Two Routes: A Structural Analysis

| Feature | KalshiEX (DCM Route) | Coinbase/Deribit (FCM Route) |

|---|---|---|

| Legal Status | Formal Commission Order | Staff Interpretation / No-Action Position |

| Product Location | Listed directly on a U.S. exchange | Listed on a foreign board of trade (Deribit) |

| Regulatory Weight | High (Formal product approval) | Moderate (Non-binding, fact-specific relief) |

| Target Audience | Domestic retail and institutional | Institutional (with retail expansion planned) |

| Collateral Rules | Cash-settled under U.S. DCM rules | Allows digital assets/stablecoins as margin (with conditions) |

The Coinbase route is particularly notable for its treatment of margin. The CFTC staff letter addresses the posting of customer-owned digital commodities and payment stablecoins as margin through foreign affiliates. This is a critical concession, as it allows for greater capital efficiency by letting traders use their existing crypto holdings as collateral, a standard practice in the offshore market that has been difficult to replicate under strict U.S. segregation rules.

Broader Impact and the Liquidity Test

While the regulatory hurdles have been cleared, the next challenge is the "liquidity test." Historically, regulated U.S. crypto products have struggled to compete with the sheer volume and high leverage (often up to 100x) offered by offshore platforms like Binance or Bybit. For the Kalshi and Coinbase initiatives to succeed, they must offer competitive funding rates, deep order books, and a seamless user experience.

The CFTC’s cautious approach—limiting the initial scope to Bitcoin—suggests a "crawl-walk-run" strategy. If the Bitcoin perpetual market proves stable and resistant to manipulation within the U.S. framework, it is highly likely that similar approvals for Ethereum (ETH) and other major digital commodities will follow.

Furthermore, this development puts pressure on the U.S. Congress to finalize comprehensive market structure legislation. While the CFTC has used its existing authority under the CEA to create these paths, a permanent legislative framework would provide the long-term certainty required for major Wall Street banks to enter the perpetuals space as market makers or clearing members.

Conclusion

The transition of Bitcoin perpetuals to U.S. soil marks the end of the "theoretical" phase of crypto onshoring. With Kalshi providing a direct domestic product and Coinbase offering a supervised gateway to global liquidity, the U.S. is positioning itself to reclaim its influence over the digital asset derivatives market. The success of these initiatives will ultimately depend on whether regulated venues can match the efficiency of the offshore world while maintaining the safety standards mandated by the CFTC. As institutional onboarding begins, the industry will be watching closely to see if the "80% of global volume" currently held offshore begins to migrate toward the transparency of U.S. regulation.