This shift in the regulatory landscape follows the implementation of the SEC’s generic listing standards in September 2025, which fundamentally altered how Commodity-Based Trust Shares are brought to market. By utilizing Commodity Futures Trading Commission (CFTC)-regulated futures on Designated Contract Markets (DCMs) as a prerequisite, issuers have found a way to bypass the lengthy and often contentious bespoke 19b-4 filing process. This transition has turned what was once a multi-year regulatory "limbo" into a predictable 75-day administrative window, provided specific infrastructure milestones are met.

The Regulatory Evolution: From Enforcement to Infrastructure

For years, the digital asset industry viewed the SEC as a gatekeeper whose primary tool was the "unregistered security" designation. XRP sat at the epicenter of this conflict following the SEC’s 2020 lawsuit against Ripple Labs. However, the resolution of that legal battle, combined with the maturation of derivatives markets, has created a new paradigm. The SEC’s approval of generic listing standards in late 2025 allows national securities exchanges to list and trade qualifying trust shares without submitting a proposed rule change for every individual asset.

The practical impact of this change is a drastic compression of approval timelines. Under the previous regime, the approval process for a crypto-linked ETF could take upwards of 240 days, often involving repeated rejections and legal challenges. Under the new "fast lane," once an asset has a CFTC-regulated futures market with at least six months of trading history, the exchange-side approval process is reduced to approximately 75 days. This shift effectively moves the "gatekeeping" power from the SEC’s legal department to the infrastructure of DCMs and benchmark administrators.

Bitnomial, a prominent DCM, recently highlighted that regulated futures have become the "new math" for ETF eligibility. The sequence is now clearly defined: launch DCM futures, accrue six months of history to establish surveillance and liquidity benchmarks, file under generic standards, and reach a listing within the quarter.

A Chronology of XRP’s Transformation

The journey of XRP from a regulatory pariah to an ETF pioneer provides a template for other altcoin ecosystems. The timeline below illustrates the critical milestones that facilitated this transition:

- December 2020: The SEC filed a lawsuit against Ripple Labs, alleging that XRP was sold as an unregistered security. This established XRP as a high-profile "regulatory risk" asset, setting the stage for a years-long legal battle.

- July 2023: A landmark court ruling determined that while certain institutional sales of XRP were securities, programmatic sales on public exchanges were not. This created the operational "breathing room" necessary for exchanges to maintain liquidity without fear of immediate enforcement.

- March 2025: Bitnomial launched the first CFTC-regulated XRP futures. This initiated the "infrastructure clock," providing the U.S.-regulated derivatives rails required by the SEC’s later standards.

- May 2025: The CME Group followed with cash-settled XRP futures tied to the CME CF XRP-Dollar Reference Rate. This added institutional-grade benchmark pricing and clearing plumbing, which are essential for satisfying surveillance-sharing requirements.

- September 2025: The SEC officially approved generic listing standards for Commodity-Based Trust Shares. Simultaneously, REX-Osprey’s XRPR debuted as the first U.S.-listed spot XRP ETF, followed shortly by Franklin Templeton’s Franklin XRP ETF (XRPZ).

- Late 2025: The Second Circuit Court officially dismissed the remaining Ripple-SEC appeals, ending the four-year legal saga with a $125 million penalty and an injunction against future institutional violations, but leaving the ETF wrapper intact.

This chronology demonstrates that XRP’s success was not based on a total regulatory "pardon," but rather on the asset’s ability to fit into a standardized product wrapper. XRP did not become "safe" in the eyes of all regulators; it became productizable.

The DCM-First Pathway: A New Industry Standard

The "assembly line" for altcoin ETFs now moves power toward entities that control market infrastructure. DCMs, derivatives clearing organizations (DCOs), and benchmark administrators like CME CF have become the kingmakers of the crypto-financial system. For a token to be considered for an ETF, it must first secure a listing on a regulated futures exchange.

This infrastructure-first approach provides several benefits to the market. First, it ensures that a robust hedging and arbitrage ecosystem exists before a spot ETF is launched. Regulated futures allow market makers to manage risk more effectively, which typically results in tighter spreads and better price discovery for the eventual spot product. Second, the six-month history requirement allows for the accumulation of data regarding market manipulation and surveillance, addressing the SEC’s long-standing concerns about the "size and significance" of regulated markets.

However, this pathway also introduces a form of "reflexivity risk." When a token foundation or issuer secures a DCM futures listing, it often triggers immediate speculative interest in a future ETF. This speculation can drive up market capitalization and liquidity, making the asset even more attractive for futures trading, thereby creating a feedback loop that accelerates the asset’s path to the ETF wrapper.

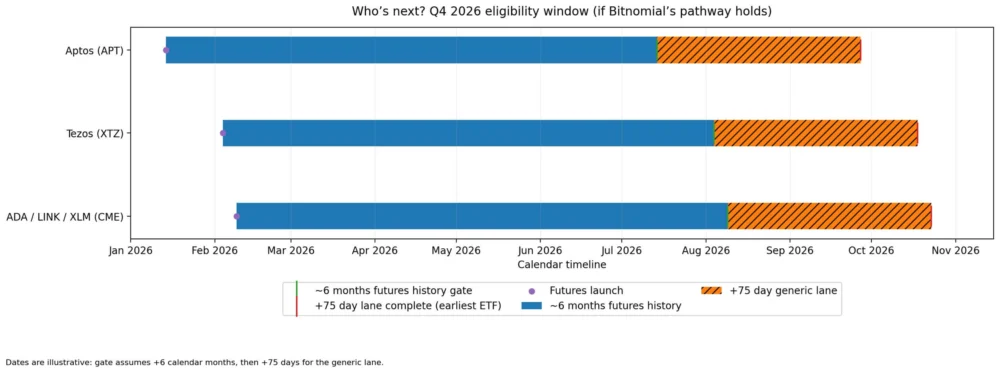

Projecting the 2026 Eligibility Window

Using the "nine-month math"—six months of futures history plus a 75-day filing period—market analysts have identified several high-profile altcoins that are poised for ETF eligibility in the latter half of 2026. The expansion of futures offerings by major exchanges like Bitnomial and CME Group serves as the primary indicator for these upcoming windows.

Aptos (APT) futures launched on Bitnomial on January 14, 2026. If the six-month maturity rule holds, the asset could see its first ETF filing in mid-2026, leading to a potential listing by late September 2026. Similarly, Tezos (XTZ) futures, which debuted on February 4, 2026, point toward an eligibility window in mid-October 2026.

The most significant cluster of potential launches involves Cardano (ADA), Chainlink (LINK), and Stellar (XLM). Following CME Group’s announcement of futures for these assets on February 9, 2026, all three tokens are on track to meet the infrastructure requirements for a late October 2026 ETF launch. CME’s move to 24/7 crypto derivatives trading, scheduled for May 29, 2026, is expected to further bolster the liquidity profiles of these assets, making them even more viable candidates for institutional wrappers.

Institutional Implications and Market Strategy

The shift from a "file and pray" strategy to an "infrastructure first" approach has fundamentally changed the incentives for token foundations. Rather than lobbying the SEC directly, foundations are now prioritizing relationships with DCMs and clearinghouses. The goal is no longer to convince a regulator of a token’s utility, but to prove its market maturity through regulated derivatives.

For institutional allocators, this development is a net positive. The presence of a futures market prior to a spot ETF provides a more familiar environment for risk management. Institutional-grade benchmarks, such as those provided by CME CF, offer a level of transparency and standardization that was previously lacking in the altcoin space.

However, the concentration of power in a small number of regulated venues remains a point of discussion. Assets that are technically incompatible with current DCM infrastructures or those with smaller market capitalizations may find themselves excluded from this expedited pathway. This could create a "two-tier" crypto market: one tier of "productizable" assets with deep institutional access, and a second tier of assets that remain confined to native crypto exchanges and decentralized finance (DeFi) protocols.

Analysis of Remaining Risks

While the procedural path has been cleared, legal and regulatory complexities remain. The XRP case showed that an asset can have an ETF even while portions of its history are still classified as securities violations. The $125 million penalty paid by Ripple and the ongoing injunction against institutional sales serve as a reminder that the ETF wrapper does not offer total legal immunity.

Furthermore, the "generic" nature of the listing standards means that the SEC still retains the authority to intervene if it identifies specific risks related to a particular asset’s underlying technology or governance. Issues such as network centralization, "kill switches" in smart contracts, or significant holdings by concentrated groups of insiders could still serve as grounds for a listing to be challenged, even if the futures-history requirement is met.

Ultimately, the transformation of XRP has demonstrated that eligibility is the primary metric for the modern financial system. Whether an asset is a "security" or a "commodity" in a philosophical sense has become less important than whether it can be safely and efficiently wrapped in a regulated vehicle. As the market moves toward late 2026, the industry will watch closely to see if the "XRP playbook" becomes the permanent manual for the next generation of digital asset products.