The Evolution of the Basel III Endgame

The current debate centers on the final implementation of the Basel III standards, an international regulatory framework developed in the wake of the 2008 global financial crisis. Often referred to as the "endgame," these rules were designed to standardize how large banks calculate their risk-weighted assets and determine the size of the capital buffers they must maintain to survive economic shocks.

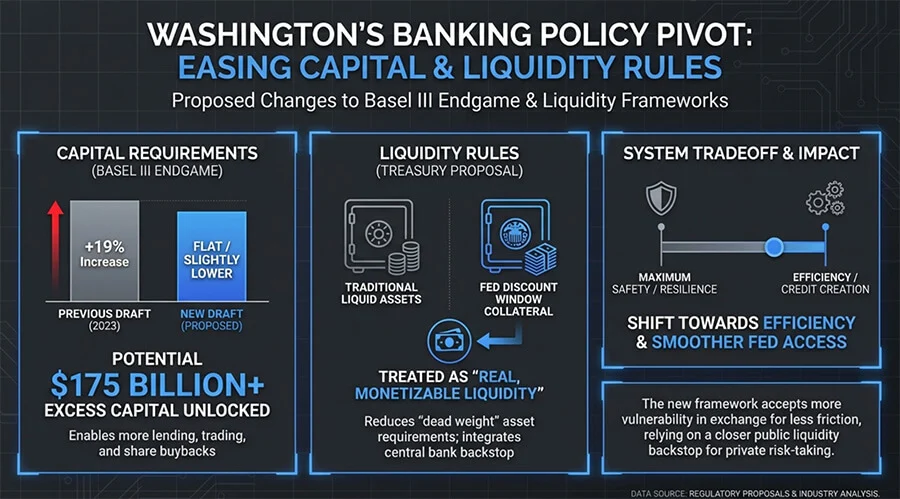

In July 2023, under the direction of Federal Reserve Vice Chair for Supervision Michael Barr, U.S. regulators proposed a version of these rules that would have increased capital requirements for the largest banks by approximately 19%. The proposal was met with an unprecedented lobbying campaign from Wall Street. Industry giants argued that the stringent requirements would stifle economic growth, make American banks less competitive globally, and force essential services like small-business lending and mortgage processing into the "shadow banking" sector, which operates with less oversight.

The new direction announced by Vice Chair Bowman suggests that the upcoming rewrite will leave capital requirements for the largest institutions roughly flat or even slightly lower than current levels. This shift represents a major victory for the banking lobby and a significant concession by the Federal Reserve, the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC).

The $175 Billion Windfall and Surcharge Reductions

The financial implications of this regulatory easing are vast. By softening the capital mandates, regulators are effectively allowing banks to move billions of dollars from "idle" safety buffers into active market use. Analysts estimate that the revised framework could free up more than $175 billion in excess capital across the U.S. banking sector.

Furthermore, the proposal includes a reduction in the surcharges applied to Global Systemically Important Banks (G-SIBs)—the elite tier of financial institutions whose failure could trigger a global meltdown. These surcharges, which are based on a bank’s size, complexity, and interconnectedness, are expected to fall by approximately 10%. For institutions like JPMorgan Chase, Bank of America, and Citigroup, this reduction translates into billions of dollars in capital that can be redirected toward share repurchases, increased dividends, or expanded trading operations.

The logic behind this reduction, according to Bowman, is to ensure that capital requirements are "aligned with actual risk." Supporters of the move argue that the 2023 proposal overshot the mark, creating a "capital drag" that penalized banks for holding low-risk assets and participating in market-making activities that provide liquidity to the broader economy.

A Fundamental Shift in Liquidity Management

While the changes to capital requirements have dominated headlines, a second, equally critical policy shift is occurring regarding bank liquidity. Liquidity refers to the cash or easy-to-sell assets a bank keeps on hand to meet immediate demands, such as customer withdrawals.

Following the regional banking crisis of early 2023, which saw the rapid demise of Silicon Valley Bank (SVB) and Signature Bank, regulators initially emphasized the need for banks to hold more high-quality liquid assets (HQLA). However, the U.S. Treasury and the Federal Reserve are now exploring a redesign of these rules. The new approach would allow banks to receive regulatory credit for collateral they have "prepositioned" at the Federal Reserve’s discount window.

The discount window is the central bank’s emergency lending facility, designed to provide liquidity to banks in times of stress. Historically, using the discount window carried a heavy "stigma"; banks feared that if the market found out they were borrowing from the Fed, it would be interpreted as a sign of imminent insolvency, potentially triggering the very bank run they were trying to avoid.

Treasury officials are now describing this borrowing capacity as "real, monetizable liquidity." By integrating the discount window more formally into the regulatory framework, the government is acknowledging that the central bank backstop is not just an emergency tool but a core component of the financial system’s plumbing. This change would allow banks to carry fewer liquid assets on their own balance sheets, provided they have assets—such as Treasury bonds or mortgage-backed securities—ready to be swapped for cash at the Fed.

Lessons from the 2023 Regional Banking Crisis

The pivot toward lighter regulation comes only three years after the failures of Silicon Valley Bank, Signature Bank, and First Republic Bank. Those collapses were characterized by a "digital bank run," where depositors moved money at speeds never before seen in the financial industry.

The Fed’s internal review of the SVB failure initially concluded that the bank suffered from critical weaknesses in risk management and that supervisors had failed to act with sufficient force. The official recommendation at the time was clear: banks needed more "thicker" buffers to withstand the volatility of the modern era.

The 2026 rewrite, however, suggests a different interpretation of those events. Rather than forcing banks to become entirely self-reliant through massive capital piles, the new framework seeks to make the existing system more flexible. It assumes that the primary failure in 2023 was not necessarily a lack of capital, but a failure of liquidity mobilization. By making the discount window easier to use and lowering capital hurdles, regulators hope to prevent "friction" from turning a localized liquidity squeeze into a systemic crisis.

Political Reactions and Rising Opposition

The proposed easing of bank rules has ignited a sharp political divide in Washington. Senator Elizabeth Warren, a long-time advocate for strict financial oversight, has emerged as one of the most vocal critics of the Fed’s new direction. Warren has warned that weakening capital standards while geopolitical tensions are high and credit risks are rising is a "dangerous mistake."

"We saw what happens when we let big banks write their own rules in 2008 and again in 2023," Warren stated in response to the reports. Critics of the plan argue that the $175 billion "break" for banks essentially shifts the burden of risk from private shareholders to the public. If a bank carries a thinner cushion and fails, the Federal Reserve and the FDIC are more likely to be forced into an emergency intervention.

Conversely, industry groups such as the American Bankers Association (ABA) and the Bank Policy Institute (BPI) have welcomed the news. They maintain that the 2023 proposal was "fatally flawed" and would have harmed consumers by raising the cost of credit. They argue that U.S. banks are already the best-capitalized in the world and that further increases would provide diminishing returns in terms of safety while causing tangible harm to economic growth.

The Bitcoin Paradox: Traditional vs. Digital Risk

The regulatory pivot is particularly striking when contrasted with Washington’s treatment of digital assets. While the Federal Reserve is moving to give traditional banks more flexibility with their capital and liquidity, it remains steadfastly restrictive regarding Bitcoin and other cryptocurrencies.

Under current guidelines, banks that choose to hold Bitcoin on their balance sheets are subject to extremely high capital charges—often requiring them to hold a dollar of capital for every dollar of Bitcoin exposure. This "punitive" treatment ensures that crypto remains on the periphery of the regulated banking system.

The contrast suggests that while regulators are becoming more comfortable backstopping traditional financial risks—such as interest rate mismatches and commercial real estate exposure—they remain unwilling to normalize Bitcoin within the banking sector. The message from Washington appears to be that the "old" system will be given more room to breathe, but the "new" system of digital finance will remain under heavy guard.

Fact-Based Analysis: The Tradeoff Between Safety and Efficiency

The decision to soften Basel III and liquidity rules is a classic exercise in balancing financial stability with economic efficiency.

- Efficiency and Growth: Lower capital requirements mean banks can lend more. Every dollar not held in a "shock absorber" buffer can be leveraged into multiple dollars of credit for businesses and consumers. This can stimulate growth, particularly in a high-interest-rate environment where borrowing costs are already elevated.

- Market Liquidity: Banks play a crucial role as market makers. When capital rules are too strict, banks reduce their activity in bond markets, making it harder for others to buy and sell securities. This can lead to "flash crashes" or extreme volatility. The new rules aim to restore this market-making capacity.

- Systemic Risk: The "slack" being introduced into the system is the primary concern for stability advocates. A $175 billion reduction in capital means the industry has $175 billion less to lose before it reaches a point of insolvency. By relying more heavily on the Fed’s discount window, the system becomes more dependent on central bank intervention.

Conclusion: Preparing for the Next Stress Event

The Federal Reserve’s decision to rewrite the Basel III endgame is a pragmatic, if controversial, acknowledgment of the limits of regulation. It suggests a belief among current leadership that the post-2008 era of ever-increasing capital mandates has reached its logical conclusion.

As Washington prepares to finalize these rules, the banking industry is poised for a period of renewed flexibility and profitability. For Wall Street, the $175 billion break is a welcome reprieve that rewards years of intensive lobbying. For the broader public, however, the changes serve as a reminder that the stability of the financial system remains a work in progress.

The ultimate test of this new framework will not come during a period of economic growth, but during the next inevitable market panic. By lowering the buffers and making the Fed’s backstop a "monetizable" part of daily operations, regulators are betting that a more agile, less-constrained banking system will be better equipped to handle the shocks of the future. Whether that bet pays off or leads to another round of taxpayer-funded rescues remains the central question for the American financial landscape.