While current indicators do not suggest an immediate, 2008-style collapse of the banking system itself, the concentration of risk within private credit funds, mortgage finance firms, and securitization vehicles creates a new set of vulnerabilities. The risk has not been eliminated; rather, it has been outsourced and layered. In this evolving environment, the primary concern is no longer a direct run on a major bank, but a "liquidity transmission" event where stress originating in private, illiquid markets works its way backward into the banking stack.

A Chronology of Credit Migration: 2010 to 2025

The shift toward non-bank lending was an unintended, though perhaps predictable, consequence of the regulatory overhaul that followed the 2008 crisis. The implementation of the Dodd-Frank Wall Street Reform and Consumer Protection Act and the global Basel III standards forced traditional banks to hold higher capital reserves and reduce their exposure to high-risk direct lending.

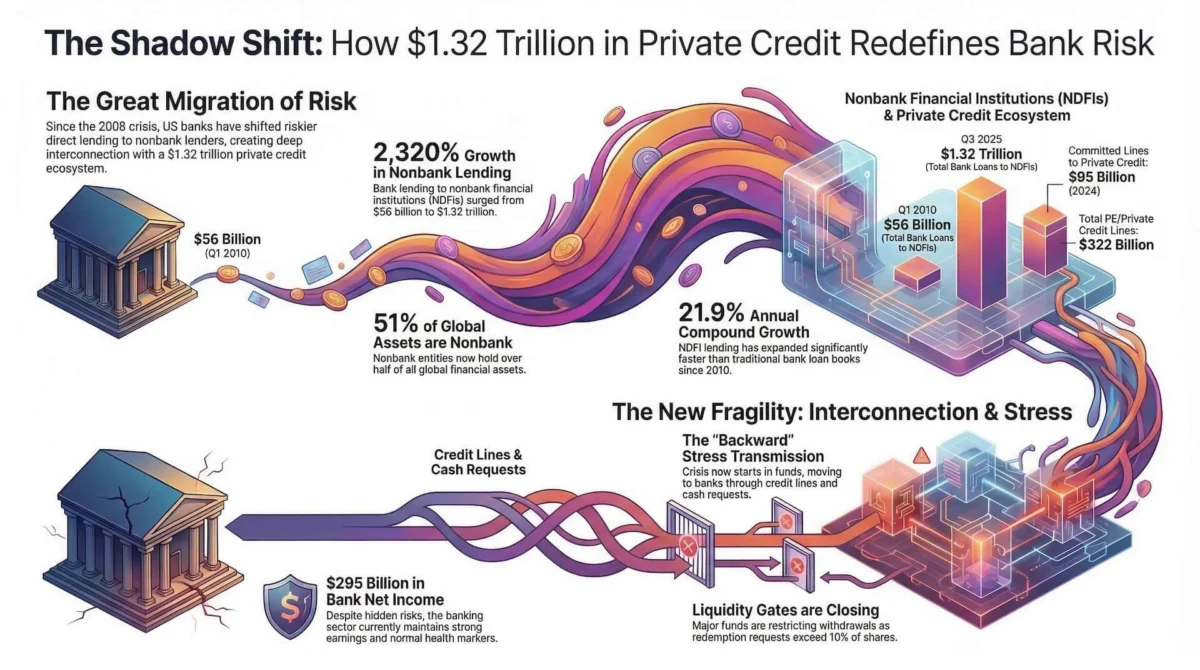

In the first quarter of 2010, bank lending to NDFIs stood at a relatively modest $56 billion. However, as traditional banks pulled back from lending to middle-market companies and riskier commercial ventures, private credit funds and other non-bank entities stepped in to fill the vacuum. By 2013, Federal Reserve data showed that committed credit lines from major banks to private credit vehicles had risen to $8 billion.

The ensuing decade saw a period of ultra-low interest rates and aggressive search for yield among institutional investors, which fueled the rapid expansion of the shadow banking sector. Between 2010 and 2024, the category of bank lending to NDFIs grew at a compound annual rate of 21.9%. By the end of 2024, total committed bank lines to private credit and private equity had ballooned to approximately $322 billion. As of the third quarter of 2025, the FDIC documented $1.32 trillion in total NDFI loans, marking a historical peak and a 23-fold increase since the post-crisis low.

Analyzing the $1.32 Trillion Exposure

The scale of this exposure is best understood through the lens of institutional interdependence. NDFIs are broad categories that include mortgage intermediaries, consumer finance firms, and private equity vehicles. Unlike traditional banks, these institutions do not take deposits and are not subject to the same level of public disclosure or capital requirements.

According to a Federal Reserve staff note, the largest US banks are now inextricably tied to the private-credit system through direct financing lines. Of the $95 billion in committed credit lines specifically designated for private-credit vehicles in late 2024, approximately $56 billion had already been drawn. This creates a feedback loop: banks provide the leverage that private credit funds use to make loans. If those loans default or if the funds face massive redemption requests from their own investors, the banks’ credit lines are the first to be impacted.

The Financial Stability Board (FSB) reported that by 2024, the non-bank financial intermediation sector accounted for approximately 51% of total global financial assets. This indicates that the US trend is part of a wider global shift where credit has migrated away from the classic banking model. The migration has been so thorough that non-bank finance is now growing at roughly twice the pace of the traditional banking sector.

Current State of the US Banking Sector

Despite the alarming growth in shadow bank exposure, the official health check of the US banking industry remains stable in the short term. The FDIC’s quarterly banking profile for the end of 2025 reported that the sector earned $295.6 billion in net income, with a return on assets (ROA) of 1.24%. Furthermore, unrealized losses on securities—a major pain point during the regional banking stress of 2023—were reduced to $306.1 billion.

The FDIC currently identifies 60 "problem banks," a figure that remains within the agency’s historical non-crisis range. These metrics suggest that the banking system is not currently in a state of panic or imminent failure. However, analysts warn that these "lagging indicators" may not capture the "leading risks" embedded in the NDFI loan book. The stability of the banks is increasingly dependent on the stability of the non-banks they finance.

Emerging Signs of Stress in Private Credit

The first cracks in the private-credit facade began to appear in late 2024 and early 2025. As interest rates remained higher for longer than many market participants anticipated, the cost of servicing private debt rose, leading to a surge in redemption requests. Several high-profile private-credit vehicles have been forced to limit or manage withdrawals to prevent a fire sale of assets.

Recent reports highlight that Cliffwater’s flagship corporate lending fund met only half of its 14% redemption requests, while Morgan Stanley’s North Haven fund honored only its 5% cap despite higher demand for exits. BlackRock and other major asset managers have also hit quarterly withdrawal limits. This illiquidity is a fundamental characteristic of private credit; assets are often held to maturity and cannot be liquidated quickly without significant "haircuts" to their value.

Simultaneously, major lenders like JPMorgan have begun to tighten terms. Reports indicate that JPMorgan recently marked down software-backed private-credit portfolios and restricted lending to specific funds. This move suggests that banks are becoming more selective and less willing to accept stale valuations of private assets as collateral for their loans.

The Role of Alternative Assets and Bitcoin

The comparison of the $1.32 trillion NDFI exposure to 18 million Bitcoin serves as a measure of scale, but it also highlights a growing narrative in the financial markets. Bitcoin, currently trading near $73,777 with a market dominance of 58.5%, is increasingly viewed as a "liquidity barometer."

In the event of a broad credit squeeze, Bitcoin’s short-term outlook is complex. Because it is one of the most liquid assets in global markets, it is often sold first to meet margin calls or cash needs elsewhere in a portfolio. However, over a longer horizon, the structural issues within the banking and shadow banking systems provide a fundamental argument for decentralized assets. If the "lending chain" of banks and NDFIs suffers a loss of trust due to opaque valuations and liquidity mismatches, the appeal of an asset with a transparent, immutable ledger and no counterparty risk becomes more pronounced.

Regulatory and Official Responses

Regulators are moving from a period of observation to one of heightened scrutiny. The FDIC has emphasized that the NDFI loan segment requires closer monitoring due to its rapid growth and the "interconnectedness" it creates between regulated banks and the shadow banking system. While the Federal Reserve concluded in a 2024 research note that direct financial-stability risk appeared "limited so far" because large banks could absorb drawdowns, they acknowledged that the opacity of non-bank lenders remains a significant blind spot.

Statements from industry leaders also suggest a shift in sentiment. The chair of Partners Group recently noted that private-credit default rates could double from their historical average of 2.6% in the coming years. While not a baseline forecast, this admission from within the industry reflects a growing recognition that the era of "benign losses" in private credit may be ending.

Broader Impact and Systemic Implications

The primary risk to the broader economy is not a sudden bank failure, but a "credit crunch" facilitated by the tightening of financing to NDFIs. If banks continue to restrict the credit lines they provide to shadow lenders, middle-market companies—which rely heavily on private credit for operations and expansion—will face higher costs and reduced access to capital.

The systemic threat is best framed as a "slow-motion" repricing. In public markets, losses are recognized instantly. In private markets, they are deferred through managed withdrawals and infrequent mark-to-market valuations. This delay creates a period of "phantom stability" that can vanish quickly if cash needs force a realization of losses.

As the market enters the next phase of the credit cycle, three factors will determine the outcome:

- The Durability of Bank Financing: Will banks maintain their $1.32 trillion exposure, or will they continue the trend of tightening collateral requirements?

- Private Fund Liquidity: Can private credit funds manage redemptions without resorting to forced asset sales that could trigger a broader market repricing?

- Borrower Quality: As refinancing windows narrow, will middle-market borrowers be able to sustain higher interest payments without a spike in defaults?

The migration of credit risk to the shadow banking system has successfully shielded the traditional banking sector from direct shocks for over a decade. However, the sheer scale of the NDFI loan book suggests that the banking system is now more connected to the "unregulated" world than at any point in history. Whether this structural shift represents a safer distribution of risk or merely a hidden accumulation of it will likely be tested in the coming fiscal year.