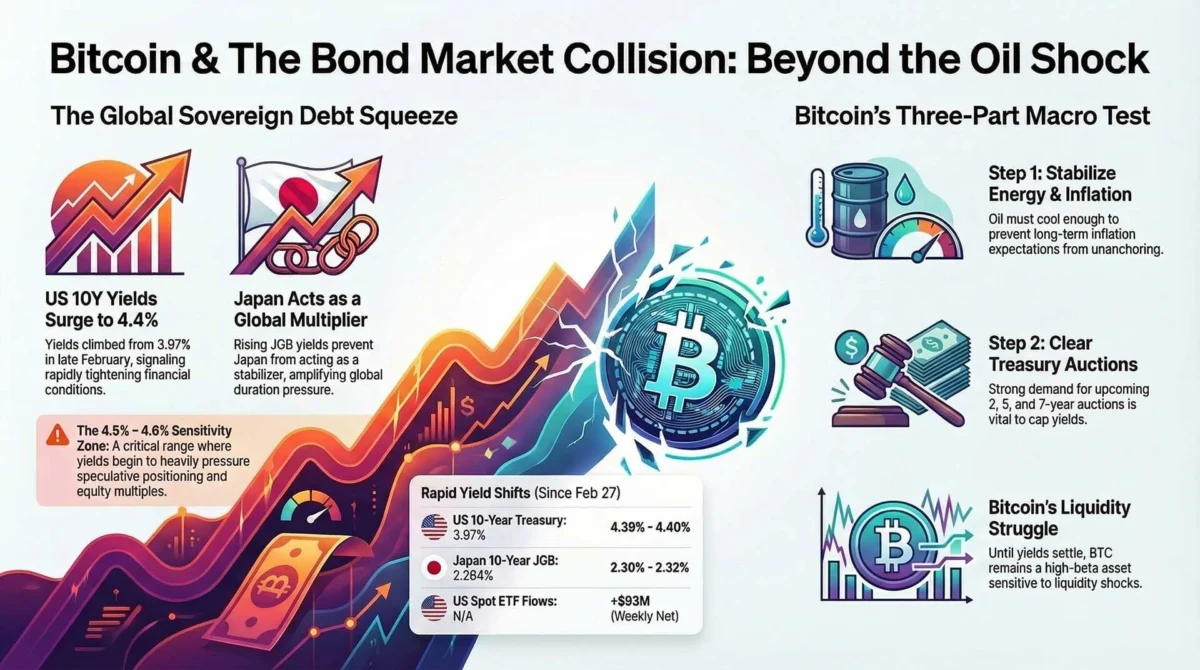

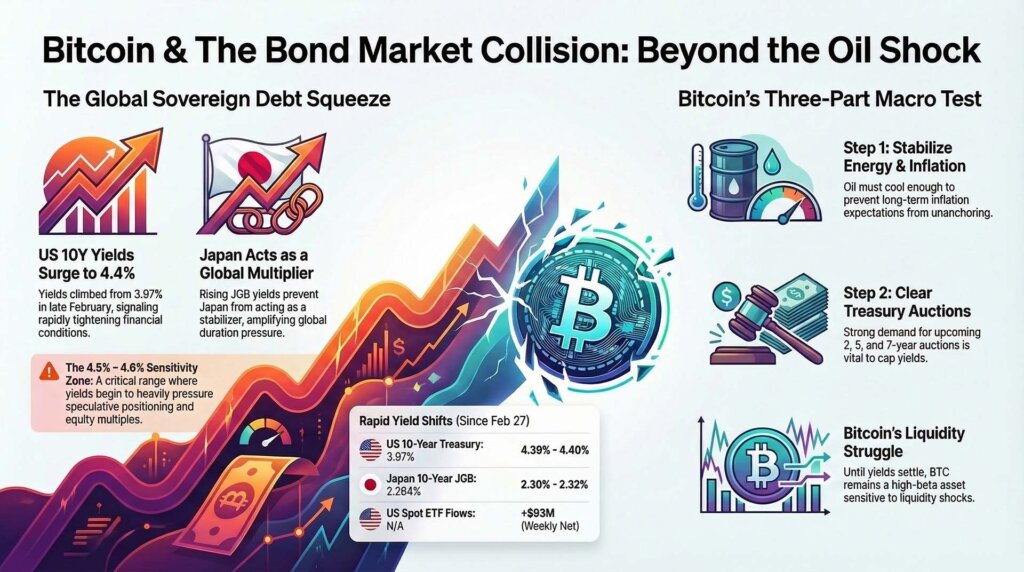

The global financial landscape is undergoing a significant transition as the primary driver of market volatility shifts from energy prices to the sovereign debt markets. While the initial macro shock was catalyzed by surging oil prices following geopolitical tensions in the Middle East, investors are now recalibrating their strategies based on the rapid ascent of bond yields in both the United States and Japan. This shift has placed Bitcoin and other risk assets in a precarious position, as the "long end" of the yield curve becomes the binding constraint for global liquidity and speculative positioning.

For much of early 2026, the market narrative was dominated by the risk of a persistent energy shock. However, as the final week of March begins, the focus has moved from the spark—oil—to the channel—bond markets. The 10-year U.S. Treasury yield and the 10-year Japanese Government Bond (JGB) yield have both experienced sharp upward moves, signaling a fundamental repricing of inflation expectations and the duration of restrictive monetary policy. Bitcoin, which continues to fluctuate between its roles as a liquidity-sensitive macro asset and a long-term hard-asset hedge, is currently trading within this bond-driven channel, reflecting the broader tension in the financial system.

The Geopolitical Spark and the Bond Market Response

The current market environment was precipitated by a geopolitical shock involving the United States and Iran, which initially sent crude oil prices higher. In the logic of macroeconomics, higher energy prices serve as a double-edged sword: they act as a tax on consumers, slowing growth, while simultaneously stoking inflation expectations. This combination complicates the decision-making process for central banks, particularly the Federal Reserve, which has been attempting to engineer a "soft landing" for the U.S. economy.

As the energy shock became more pronounced, the bond market began to price in the likelihood that inflation would remain "sticky" for longer than previously anticipated. This resulted in a sharp selloff in sovereign debt, pushing yields higher. The U.S. 10-year Treasury yield, a global benchmark for the cost of capital, stood at 3.97% on February 27. Following the escalation of conflict and the subsequent rise in oil prices, the yield climbed to 4.39% by March 20. By the start of trading on Monday, March 23, the yield was testing the 4.4% threshold, a level that exerts significant pressure on equity valuations and high-beta assets like Bitcoin.

The Kobeissi Letter, a prominent macro-economic commentary, highlighted this shift, noting that while oil prices remain a threat, the bond market is now the primary arbiter of how long the U.S. can maintain its current geopolitical and economic posture. The mechanics are clear: if yields continue to rise, the cost of financing government debt increases, and financial conditions tighten autonomously, potentially forcing the hand of policymakers.

Chronology of the Macro Shift: February to March 2026

The transition from an energy-focused market to a yield-focused market can be traced through a series of key events and data releases over the past four weeks:

- February 27-28: Geopolitical tensions in the Middle East escalate. Crude oil prices begin to climb, and the U.S. 10-year yield sits at sub-4% levels.

- March 12: The U.S. Bureau of Labor Statistics releases February CPI data. Headline inflation comes in at 2.4% year-over-year, with core CPI at 2.5%. The data suggests that inflation is not cooling as quickly as the Federal Reserve might prefer.

- March 13: February PPI (Producer Price Index) runs hotter than expected on a monthly basis, signaling that inflationary pressures are moving through the supply chain.

- March 18: The Federal Reserve holds interest rates steady at 3.50% to 3.75%. Chair Jerome Powell notes that the situation in the Middle East adds a layer of uncertainty to the policy outlook, but provides no immediate signal of a pivot toward easing.

- March 20: The U.S. 10-year yield hits 4.39%. Simultaneously, Japanese 10-year JGB yields rise to 2.264%. U.S. spot Bitcoin ETFs record a net positive flow of $93 million for the week, though momentum slows in the final sessions.

- March 23 (Early Session): Yields in the U.S. and Japan continue to press upward. Reports emerge that Japan is considering trimming buybacks of inflation-linked bonds, further spooking the debt markets.

- March 23 (11:23 GMT): A sudden diplomatic shift occurs. Former President Trump issues a statement claiming "productive conversations" regarding a resolution of hostilities with Iran. Bitcoin reacts instantly with a 4.5% jump, illustrating the asset’s extreme sensitivity to geopolitical de-escalation.

The Japan Factor: A Global Repricing of Risk

One of the most critical developments in the current macro landscape is the involvement of the Japanese government bond market. Historically, Japan has served as a source of low-cost liquidity for the global financial system through the "carry trade." However, as Japanese inflation expectations stir, the Bank of Japan (BOJ) is being forced to reconsider its ultra-accommodative stance.

The 10-year JGB yield rose from 2.264% on Friday to a range of 2.30% to 2.32% by Monday morning. Longer-dated yields, including the 30-year and 40-year JGBs, also faced upward pressure. This global synchronization of rising yields is significant; when JGBs reprice higher alongside U.S. Treasuries, it suggests that the market is treating the current shock as a systemic global event rather than a localized energy crisis.

The BOJ recently acknowledged that rising crude prices are placing upward pressure on consumer prices. Furthermore, the market is pricing in the possibility of another rate hike from the BOJ, especially as the central bank signals it may reduce its intervention in the bond market. For Bitcoin, this is a "hostile backdrop." Rising yields in Japan can lead to a repatriation of capital, further tightening global liquidity and reducing the appetite for speculative assets.

Bitcoin’s Performance Amid Liquidity Constraints

Bitcoin’s price action during this period has challenged the narrative that it serves as a "safe haven" during geopolitical strife. When the initial oil shock hit, Bitcoin did not behave like digital gold; instead, it was sold off alongside other risk assets. This response indicates that in the first stage of a liquidity shock, Bitcoin remains highly sensitive to the "cost of money."

As yields rise, the "term premium"—the extra compensation investors demand for holding long-term debt—increases. This process is generally negative for assets that do not produce cash flows, as the opportunity cost of holding them rises. Bitcoin traders found themselves caught in a "yield zone" between 4.50% and 4.60% on the U.S. 10-year, a range that many analysts consider a critical threshold for risk-asset stability.

Despite the price volatility, Bitcoin’s internal market structure has shown resilience. U.S. spot ETF flows remained net positive through the week ending March 20, and the futures basis—the difference between the spot price and the futures price—stayed positive. This suggests that while macro conditions are difficult, institutional interest has not evaporated. Instead, investors are waiting for clarity on the interest rate trajectory.

The Three-Part Macro Test for the Week Ahead

As the market enters a critical week, Bitcoin faces a three-part test that will likely determine its price trajectory for the remainder of the month. Because the February PCE inflation data (the Fed’s preferred gauge) has been delayed until April 9, the market will rely on secondary signals to gauge the health of the economy.

- Treasury Auctions and Demand: The U.S. Treasury is scheduled to auction 2-year, 5-year, and 7-year notes this week. If these auctions see weak demand, it will push yields higher, placing further pressure on Bitcoin. Conversely, strong demand would signal that investors believe yields have peaked, providing a relief rally for risk assets.

- Economic Activity Data: Tuesday’s flash PMI (Purchasing Managers’ Index) data will provide an early look at whether the energy shock is beginning to cause a contraction in business activity. If growth signals soften significantly, the market may begin to price in a "growth hit" that eventually forces yields lower, which could be constructive for Bitcoin.

- Inflation Expectations: Friday’s University of Michigan consumer sentiment reading will include updated inflation expectations. If consumers believe inflation is becoming entrenched due to high gasoline prices, it will reinforce the "higher-for-longer" interest rate narrative.

Implications and Market Outlook

The sudden 4.5% jump in Bitcoin following the news of potential diplomatic progress between the U.S. and Iran underscores the "geopolitical premium" currently baked into the market. However, the fundamental pressure from the bond market remains. Until the 10-year Treasury yield stabilizes or retreats from the 4.4% level, Bitcoin is likely to continue trading as a high-beta macro asset, tethered to the fluctuations of the sovereign debt market.

The broader implication is that the era of decoupled crypto markets is largely over. Bitcoin is now an integral part of the global macro portfolio, reacting in real-time to shifts in central bank policy, global yields, and geopolitical stability. The shift from oil to bonds as the primary market driver signifies a more mature—but also more complex—trading environment.

In conclusion, while oil may have started the current "fire" in the financial markets, the bond market is determining how far that fire will spread. Japan’s transition away from its role as a global liquidity stabilizer adds another layer of risk. For Bitcoin to reclaim its bullish momentum, it will need to see a stabilization in global yields and a decoupling from the immediate liquidity pressures that have defined the month of March. Until then, the "yield zone" remains the most important chart for every Bitcoin trader to watch.