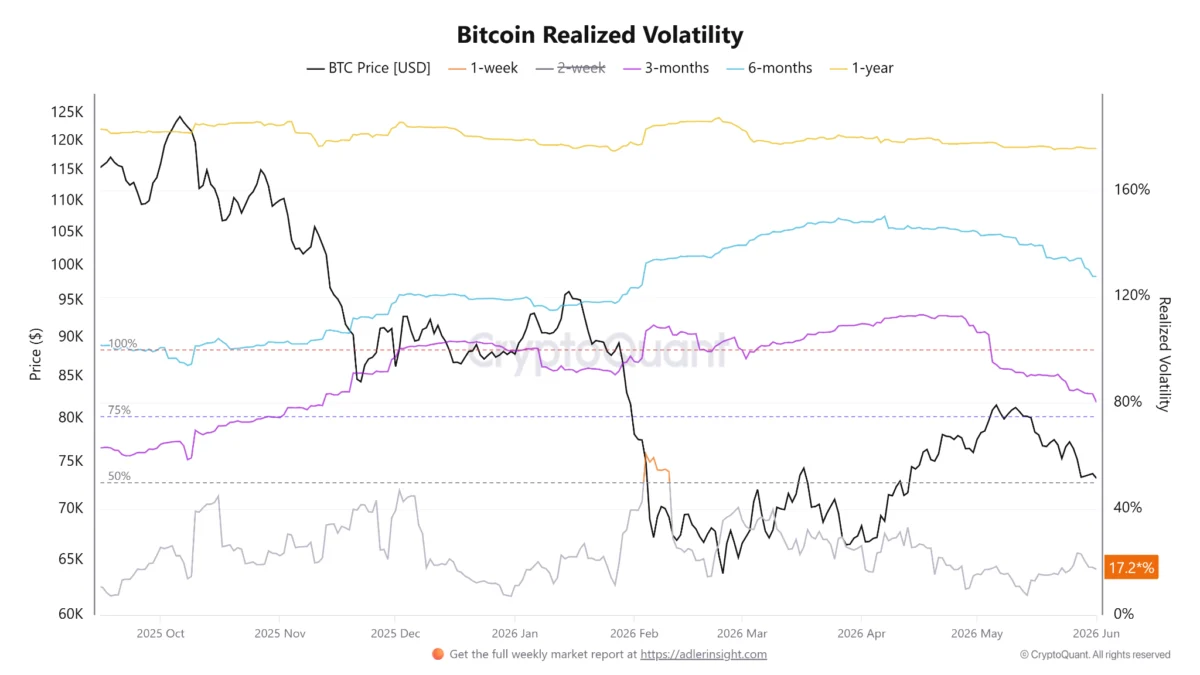

The global cryptocurrency market witnessed a notable surge on Wednesday as Bitcoin (BTC) climbed to a four-week high, sparking discussions regarding a potential return to the significant monthly close of $78,700 recorded in January. Despite a robust 22% rally from the local bottom of $60,000 established on February 6, the underlying market structure remains fragile. A comprehensive analysis of on-chain data and derivatives metrics indicates that professional traders and institutional participants maintain a cautious, if not outright bearish, stance. This hesitation persists even as the price hovers above the $73,000 threshold, suggesting that the path to a full-scale recovery is fraught with technical and psychological obstacles.

The current price action represents a significant bounce from the volatility experienced in the first week of February, during which Bitcoin suffered a 32% drawdown. While the recent recovery has injected some optimism into retail circles, the derivatives market tells a different story. Demand for downside protection, commonly referred to as "hedging," continues to dominate the landscape. Professional traders appear to be bracing for further volatility rather than positioning for an immediate breakout to new all-time highs.

The Derivatives Divide: Hedging vs. Speculation

A primary indicator of the prevailing market sentiment is the 30-day options skew, which measures the price difference between put (sell) options and call (buy) options. According to data from Laevitas.ch, put options have recently traded at a 10% premium relative to equivalent call instruments. In a balanced or "neutral" market, this indicator typically fluctuates between -6% and 6%. The current 10% skew reflects a significant lean toward bearish protection, a level of concern not seen since mid-January when Bitcoin was trading significantly higher, near the $95,000 mark.

The reluctance of professional traders is further evidenced by the stagnant demand for bullish BTC futures. The annualized premium, also known as the basis rate, currently sits below the neutral 5% threshold. This metric measures the difference between long-term futures contracts and the current spot price. When the basis rate is low, it suggests that leveraged buyers are unwilling to pay a premium to hold long positions, indicating a lack of conviction in the sustainability of the current rally. This weakness in derivatives is a direct reflection of the month-long consolidation phase that followed the early February crash, leaving many market participants skeptical of "fake-out" rallies.

On-Chain Realities and the "Underwater" Supply

The hesitation among investors is not merely psychological; it is rooted in the financial reality of the current holder base. On-chain data from Glassnode reveals a sobering statistic: approximately 43% of the circulating Bitcoin supply is currently held at a loss. This figure is calculated based on the price at which each coin last moved on the blockchain. This "underwater" supply has increased significantly since late January, when only 30% of holders were in the red while Bitcoin traded at $90,000.

This concentration of losses creates a phenomenon known as "overhead sell pressure." As the price of Bitcoin recovers toward the entry points of these investors, many are expected to sell their holdings to "break even" after weeks of unrealized losses. This behavior creates a ceiling for price appreciation, as every incremental move upward is met with a wave of sell orders from investors looking to exit the market without a loss. For Bitcoin to reclaim its previous highs, it must first absorb this massive volume of potential sell-side liquidity, a process that typically requires significant and sustained buy-side demand.

The Mining Sector Pivot: From Hashing to Artificial Intelligence

Adding to the complexity of the current market is a structural shift within the Bitcoin mining industry. Traditionally, miners have been the staunchest "HODLers" of Bitcoin, often maintaining large strategic reserves. However, the sector is currently facing a dual crisis: skyrocketing energy costs and a decline in the demand for Bitcoin blockchain transactions. This has pushed miner profitability, or "hashprice," toward historical lows.

The Bitcoin Hashprice index, which quantifies the expected daily value of one terahash per second (TH/s) of hashing power, plummeted to $30 this week, down from $39 just three months ago. In response to these dwindling margins, several major publicly traded mining firms have begun to pivot their business models. The exponential growth in demand for Artificial Intelligence (AI) and High-Performance Computing (HPC) has offered a more lucrative alternative for firms with massive data center infrastructure and power contracts.

Companies like MARA (formerly Marathon Digital Holdings) and other industry leaders have faced scrutiny over reports of offloading their Bitcoin holdings to fund this transition. While MARA executives have pushed back on the narrative that they are abandoning their Bitcoin treasury strategy, the broader trend is undeniable. Mining firms that were once net accumulators are increasingly becoming net sellers or, at the very least, diverting capital away from expanding their Bitcoin mining operations in favor of AI computing. This shift reduces the "natural" buy pressure usually provided by the mining sector and introduces a new source of potential selling as firms reallocate capital.

The $76,000 Threshold: Corporate Treasuries and Market Momentum

The role of institutional and corporate holders has become a central pillar of Bitcoin’s valuation. Strategy (MSTR), the largest corporate holder of Bitcoin, remains the bellwether for this trend. With a total holding of 720,737 BTC acquired since August 2020, the company’s average acquisition price sits at approximately $76,000. When Bitcoin trades below this level, the company’s primary asset is valued at a loss, which can impact its stock price and its ability to raise capital.

Other entities, such as Metaplanet in Japan and Twenty One Capital in the United States, have faced similar challenges during the recent market downturn. The $76,000 mark has evolved into a critical psychological and technical "line in the sand." For bears, keeping the price below this cost basis is a strategic goal; it limits the ability of these companies to issue new stock at a premium to buy more Bitcoin. Conversely, for bulls, breaking above $76,000 would validate the corporate treasury model and likely trigger a fresh wave of institutional momentum.

While Strategy does not face immediate liquidation risks—largely due to its long-term debt structure and the performance of yield-bearing assets like STRC—the market recognizes that prices above the cost basis provide a green light for further accretive acquisitions. Therefore, the region between the current price of $73,000 and the January monthly close of $78,700 is expected to be a zone of intense volatility and competition between long and short positions.

Chronology of the Current Market Cycle

To understand the present caution, one must look at the timeline of events leading into late February:

- Late January: Bitcoin hits a peak near $95,000, with only 30% of the supply in a loss position.

- February 1-6: A sharp 32% correction occurs, fueled by macroeconomic uncertainty and liquidations, bottoming at $60,000.

- February 7-20: A period of "choppy" consolidation as the market digests the crash.

- February 21-25: Bitcoin begins a slow recovery, reclaiming the $70,000 level.

- February 26 (Wednesday): Bitcoin hits a four-week high above $73,000, yet derivatives indicators remain bearish.

Analysis of Broader Implications

The current state of the Bitcoin market reflects a transition from retail-driven speculation to a more complex, institutionally influenced environment. The lack of "bullish conviction" despite rising prices suggests that the market is in a "show me" phase. Investors are no longer satisfied with mere price appreciation; they are looking for a fundamental shift in the supply-demand dynamics, particularly regarding the absorption of "underwater" coins and the stability of the mining sector.

The pivot toward AI by mining companies is perhaps the most significant long-term development. If Bitcoin mining becomes a secondary business for these firms, the security of the network remains robust, but the traditional "miner cycle" of accumulation and selling may be permanently altered. This decoupling could lead to a more stable, albeit slower-growing, asset class.

Furthermore, the concentration of corporate holdings around the $76,000 mark means that Bitcoin is no longer just a digital currency; it is a core component of several major balance sheets. This creates a feedback loop where Bitcoin’s price directly influences the equity markets, and vice versa. As the market approaches the end of the first quarter, the ability of Bitcoin to close above $78,700 will be viewed as a definitive signal of whether the bull market has resumed or if the current rally was merely a "dead cat bounce" within a larger corrective phase.

In conclusion, while the four-week high is a positive technical development, the confluence of high options skew, low futures premiums, a large percentage of holders at a loss, and a struggling mining sector suggests that the road to $80,000 and beyond will be met with significant resistance. Market participants are advised to monitor the $76,000 corporate cost basis and the $78,700 monthly close level as the primary indicators of a true shift in momentum.