The Current State of British Fiscal Health

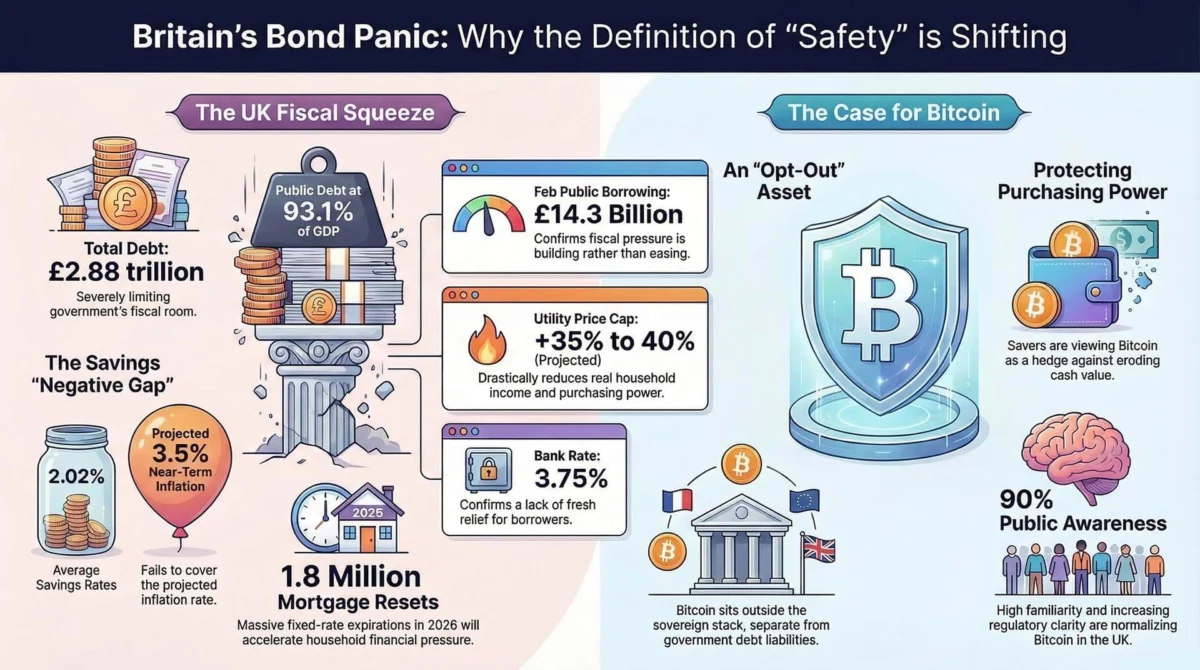

The scale of the United Kingdom’s financial challenge was brought into sharp relief by the latest official borrowing data. In February, public sector net borrowing reached £14.3 billion. This figure represents a £2.2 billion increase from the previous year and stands as the second-highest February reading since the Office for National Statistics (ONS) began keeping records in 1993. This surge in borrowing underscores a persistent gap between government spending and revenue, exacerbated by the rising costs of servicing existing debt.

As of early 2026, the total public sector net debt has reached a staggering £2.88 trillion, which accounts for approximately 93.1% of the nation’s Gross Domestic Product (GDP). This level of leverage leaves the government with minimal "fiscal headroom" to respond to new economic shocks without risking further market instability. The situation is compounded by the Bank of England’s (BoE) recent decision to maintain the Bank Rate at 3.75%, accompanied by a stark warning that energy price fluctuations are likely to push inflation higher in the coming quarters.

A Chronology of the UK’s Economic Tightening

To understand the current "bond panic," one must look at the sequence of events that led to this juncture. The UK economy has faced a series of compounding pressures over the last several years:

- The 2022 Gilt Market Crisis: The "Mini-Budget" of September 2022 served as a precursor to the current anxiety, demonstrating how quickly trust in sovereign debt can evaporate when fiscal policy is perceived as unsustainable.

- The Persistence of Inflation: Throughout 2023 and 2024, the UK struggled with higher-than-average inflation compared to its G7 peers, leading to a protracted cycle of interest rate hikes.

- The Energy Shock Redux: By late 2025, geopolitical tensions and supply chain disruptions renewed pressure on energy prices. Brent crude and Dutch TTF gas prices remained 60% above pre-shock levels, forcing the BoE to revise its inflation outlook upward.

- The March 2026 Policy Meeting: The Bank of England’s most recent minutes revealed a staff estimate for Consumer Price Index (CPI) inflation to sit between 3% and 3.5% for the foreseeable future, effectively ending hopes for an immediate pivot to lower rates.

The Erosion of Purchasing Power and the "Safety" Paradox

For the average British saver, the intersection of monetary policy and inflation has created a scenario of "financial repression." Data from the Bank of England shows that by January, the average interest rate on household instant-access deposits was a mere 2.02%. When measured against the projected inflation range of 3% to 3.5%, it becomes clear that cash held in traditional bank accounts is losing real value at a rate of approximately 1% to 1.5% per year.

While cash is traditionally viewed as the "safest" asset because it protects nominal value (the number of pounds in an account remains the same), it is failing to protect purchasing power. This discrepancy is where the definition of safety begins to shift. For decades, the "sovereign stack"—consisting of government bonds (gilts) and cash—was the bedrock of a conservative portfolio. However, as gilts become more volatile and cash yields remain below inflation, the perceived risk profile of these assets is being re-evaluated.

The Mortgage Cliff and Household Vulnerability

The macro-economic data is rapidly translating into household-level financial distress. UK Finance forecasts indicate that approximately 1.8 million fixed-rate mortgages are set to expire in 2026. These households, many of whom secured rates during the era of near-zero interest, are now facing a "mortgage cliff" as they transition to rates reflecting the current 3.75% Bank Rate plus lender margins.

The ONS Household Costs Index already indicated that by the end of 2025, inflation was running at 3.7% for mortgagors. With the Bank of England warning that the Ofgem energy price cap could rise by another 35% to 40% based on gas futures, the disposable income of millions of Britons is under direct threat. This environment creates a psychological shift: when the state-managed monetary system results in higher bills, higher taxes, and lower savings value, the appetite for an "opt-out" mechanism increases.

Bitcoin as a Non-Sovereign Alternative

Bitcoin was famously conceived in the aftermath of the 2008 financial crisis, with its Genesis Block containing a reference to the British Chancellor of the Exchequer’s second bailout for banks. The current UK situation mirrors the conditions that Bitcoin was designed to address: a high-debt sovereign state struggling to balance inflation control with debt affordability.

Bitcoin’s relevance in this context is not necessarily as a high-growth speculative vehicle, but as a "neutral" asset that sits outside the liabilities of the British state. Unlike gilts, which are promises by a government to pay back borrowed money in a currency that the government itself controls, Bitcoin has a fixed supply and no central issuer.

Critics often point to Bitcoin’s volatility as a disqualifier for its status as a safe haven. Indeed, Bitcoin experienced a 50% decline between October 2025 and February 2026, coinciding with a spike in options volatility. During periods of acute liquidity stress, investors often sell volatile assets to cover margins or raise cash. However, the long-term case for Bitcoin in the UK rests on the idea that it offers a different source of risk. While Bitcoin is subject to market volatility, it is not subject to the fiscal mismanagement or currency debasement risks inherent in sovereign debt.

Official Responses and Regulatory Context

The regulatory environment in the UK has evolved to accommodate this growing interest. The Financial Conduct Authority (FCA) recently published consumer research showing that crypto-asset awareness among the British public has exceeded 90%. Furthermore, 25% of crypto users indicated they would increase their exposure if the market were more clearly regulated. This suggests that Bitcoin is moving from the fringes of the financial system into a more formalized role within the household portfolio.

Conversely, the Office for Budget Responsibility (OBR) continues to paint a sobering picture of the UK’s fiscal future. In its March 2026 outlook, the OBR projected that 10-year gilt yields would hover around 4.5%, with 30-year yields reaching 5.3%. Perhaps most concerning is the projection that public sector net debt will continue to rise, reaching 96.5% of GDP by the 2028-29 fiscal year. The OBR also anticipates the national tax burden rising to 38% of GDP by 2030-31, the highest level in the post-war era.

Analysis of Future Scenarios

The trajectory of the UK economy over the next 12 months will likely dictate how prominently Bitcoin features in the national financial conversation. Three primary scenarios emerge:

1. The "Higher for Longer" Stabilization

In this scenario, inflation stays within the 3% range, and the Bank of England maintains rates to prevent a wage-price spiral. While the immediate panic subsides, the "slow burn" of negative real returns on cash continues. Here, Bitcoin gains ground as a narrative hedge, a way for savers to diversify away from a currency that is slowly losing its utility as a store of value.

2. The Persistent Energy Shock

Modeled by the National Institute of Economic and Social Research (NIESR), a persistent energy shock would see UK inflation run nearly 1% higher than baseline, with GDP growth slowing significantly. This "stagflationary" environment is the most potent catalyst for Bitcoin adoption, as it proves that traditional monetary tools (interest rate hikes) are struggling to contain costs that are driven by supply-side issues rather than excess demand.

3. The Financial Stability Event

The most extreme scenario involves a "duration shock" in the gilt market, where the rapid repricing of bonds threatens the solvency of institutional holders, such as pension funds. In such a case, the Bank of England might be forced to intervene with "market-functioning support"—effectively printing money to buy bonds even while inflation remains high. This institutional contradiction is precisely the scenario Bitcoin was built for, highlighting the conflict of interest inherent in central banking.

Broader Implications for Global Markets

Britain’s bond market stress serves as a "canary in the coal mine" for other highly leveraged Western economies. While the United States remains the primary driver of Bitcoin liquidity and institutional adoption via ETFs, the UK provides a clearer view of how fiscal pressure affects the individual household.

The British experience demonstrates that the case for Bitcoin is often built on the failures of the traditional system rather than the successes of the new one. When a state’s borrowing surprises on the upside, utility bills skyrocket, and the "safe" return on savings is negative in real terms, the social meaning of safety changes. The debate moves away from technical charts and toward the practical necessity of preserving purchasing power in an era of sovereign instability.

As the UK enters the second half of 2026, the data remains the primary witness: £14.3 billion in monthly borrowing and a debt-to-GDP ratio nearing 100% are not just abstract numbers. They are the indicators of a system under duress, making the case for a decentralized, non-sovereign alternative more compelling to those who had previously forgotten the origins of the Bitcoin protocol.