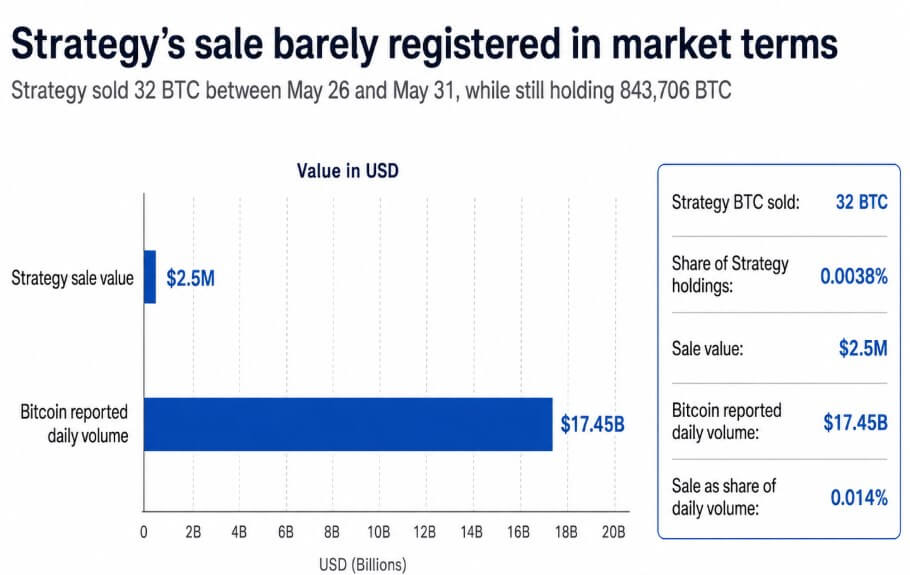

In a move that has sent ripples through the cryptocurrency markets, MicroStrategy, the enterprise software firm turned Bitcoin development company, disclosed a marginal sale of its Bitcoin holdings, sparking a disproportionate reaction among traders and analysts. According to a June 1 Form 8-K filing with the Securities and Exchange Commission (SEC), the company liquidated 32 BTC between May 26 and May 31. The sale, executed at an average net price of approximately $77,135 per coin, generated $2.5 million in proceeds. While the nominal value of the transaction is negligible relative to the company’s total treasury, the symbolic weight of the "permanent holder" selling any amount of its core asset has forced a re-evaluation of the corporate treasury model.

The MicroStrategy Disclosure: Statistical Noise vs. Narrative Impact

The $2.5 million sale was specifically earmarked to fund distributions for the company’s preferred stock, a financial obligation that requires liquid capital. As of May 31, MicroStrategy’s total Bitcoin holdings stood at a staggering 843,706 BTC. Mathematically, the 32 BTC sold represented a mere 0.0038% of the company’s total reserves. Furthermore, when compared to the broader market liquidity, the sale accounted for roughly 0.014% of Bitcoin’s reported daily trading volume of $17.45 billion on the day of the disclosure.

Despite the statistical insignificance of the trade, Bitcoin’s price fell below the $71,500 threshold shortly after the filing became public. Market observers suggest that the sell-off was less about the supply-side pressure of 32 BTC and more about the erosion of a long-held narrative. Since Michael Saylor, MicroStrategy’s Executive Chairman, began his aggressive acquisition strategy in August 2020, the company has positioned itself as a "black hole" for Bitcoin—an entity that only accumulates and never distributes. This reputation for structural buying provided a psychological floor for many institutional and retail investors. The revelation that the company would sell Bitcoin to meet operational or financial obligations introduced a new variable into the market’s conviction: even the most diamond-handed corporate treasuries have a price or a necessity that triggers a sale.

A Comparative Analysis: The Real Sellers of May

While MicroStrategy became the face of the recent market anxiety, a broader look at institutional data reveals that other public companies were significantly more active in reducing their Bitcoin exposure during the month of May. Data from BitcoinTreasuries indicates that public company reductions totaled approximately 7,500 BTC throughout the month. Interestingly, MicroStrategy’s 32 BTC sale was not even the primary driver within its own sector, and because of the June 1 filing date, it was technically categorized in the following month’s tally by some analysts.

The heavy lifting of the May sell-side pressure came from four major players: Marathon Digital Holdings (MARA), Core Scientific, Sequans, and Prenetics. Combined, these entities shed 7,359 BTC, valued at approximately $541 million based on Bitcoin’s May 31 price of $73,579. This collective reduction was roughly 230 times the size of MicroStrategy’s sale.

| Company | BTC Reduction | Approx. Value (at $73,579) | Primary Driver |

|---|---|---|---|

| Marathon Digital (MARA) | 3,386 BTC | ~$249 Million | March note repurchase activity |

| Core Scientific | 1,990 BTC | ~$146 Million | Post-bankruptcy reporting adjustments |

| Sequans | 1,481 BTC | ~$109 Million | Debt redemption/Strategy unwind |

| Prenetics | 502 BTC | ~$37 Million | Full exit to fund health business |

| Total | 7,359 BTC | ~$541 Million | Non-coordinated corporate liquidations |

The motivations behind these sales vary significantly, suggesting that there was no coordinated "dump" by corporate America. Marathon Digital’s reduction was linked to a disclosure from March regarding the funding of $1 billion in convertible-note repurchases. Core Scientific’s numbers were influenced by a change in reporting methodology following its emergence from bankruptcy, incorporating backdated entries that would not have appeared under previous tracking methods. Sequans was reportedly unwinding a failed treasury strategy to redeem outstanding debt, while Prenetics made a strategic pivot, exiting its Bitcoin position entirely to redirect capital toward its IM8 health business.

The ETF Factor: A Multi-Billion Dollar Exodus

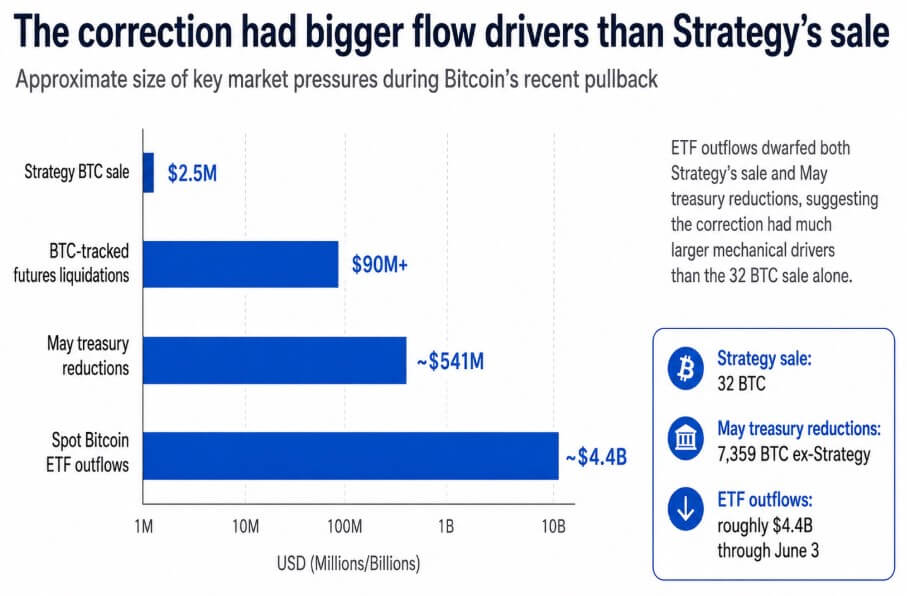

To attribute the recent 12% weekly decline in Bitcoin solely to corporate treasury adjustments is to overlook the much larger movements in the U.S. spot Bitcoin Exchange-Traded Fund (ETF) market. While corporate sales totaled half a billion dollars, U.S.-traded spot ETFs experienced a staggering $4.4 billion in outflows over a 13-day trading period ending June 3.

These outflows represent a significant shift in sentiment among institutional and retail investors who gain exposure to Bitcoin through traditional brokerage accounts. The scale of the ETF exodus is an order of magnitude larger than the combined sales of MicroStrategy and the mining firms. When $4.4 billion in liquidity is removed from the market in less than three weeks, the downward pressure on price is structural rather than narrative. This suggests that the market was already in a fragile, "risk-off" state, making it hypersensitive to the MicroStrategy headline.

Macroeconomic and Geopolitical Headwinds

The anatomy of the recent correction is further complicated by external macroeconomic factors. Geopolitical tensions in the Middle East, specifically those involving Iran, triggered a broader flight to safety in global markets. Traditionally, Bitcoin has fluctuated between being viewed as "digital gold" (a safe haven) and a "high-beta risk asset." During the latest bout of tension, it behaved firmly as the latter, declining alongside equities as investors moved toward the U.S. dollar and actual bullion.

This macro-driven decline was amplified by the derivatives market. Data shows that over $90 million in Bitcoin-tracked futures were liquidated in a single hour as the price broke key technical support levels. These forced liquidations create a cascading effect: as prices drop, leveraged long positions are closed automatically, which in turn triggers further price drops and more liquidations. In this environment, the MicroStrategy 8-K filing acted as a "narrative accelerant," providing a convenient explanation for a move that was already being driven by massive ETF outflows and geopolitical instability.

Understanding the "Saylor Premium" and Corporate Obligations

The market’s reaction to a 32 BTC sale highlights the unique position MicroStrategy holds in the ecosystem. Since 2020, the company’s stock (MSTR) has often traded at a significant premium to its Net Asset Value (NAV)—the actual value of the Bitcoin it holds. This premium exists because investors view MSTR as a leveraged bet on Bitcoin with the added security of a management team committed to never selling.

However, the 32 BTC sale reminded investors that MicroStrategy is a complex corporate entity with debt and preferred stock obligations. These instruments carry fixed distributions and maturity dates. If Bitcoin prices remain stagnant or fall while the company’s operating cash flow from its software division remains flat, the firm must find ways to service its obligations. The June 1 disclosure confirmed that management is willing to use its Bitcoin treasury as a functional balance sheet tool rather than a static trophy.

For traders, this means the "permanent buyer" model must be adjusted. While MicroStrategy remains a net accumulator—having added over 51,000 BTC recently before the minor May reductions—the "occasional seller" variable is now on the table. This repricing of expectations does not require a large-scale liquidation to impact the stock’s premium; the mere possibility of recurring sales during quarterly distribution windows is enough to cause a shift in valuation models.

Institutional Outlook and Long-Term Implications

Despite the recent drawdown and the noise surrounding MicroStrategy, some of the world’s leading financial institutions remain bullish. Geoffrey Kendrick, an analyst at Standard Chartered, maintained his $100,000 year-end price target for Bitcoin following the decline. Kendrick characterized the current volatility as a "positioning reset" rather than a fundamental break in the bull market.

For the corporate treasury model to remain viable in the eyes of investors, the next few months will be a period of proof. The market needs to see that the ETF outflow cycle has reached exhaustion and that net treasury accumulation remains positive. If MicroStrategy returns to its aggressive buying pattern in the next quarter, the 32 BTC sale will likely be remembered as a minor footnote in corporate governance.

However, if other debt-laden firms follow suit and begin selling to cover interest payments or operational costs, the narrative of Bitcoin as a structural corporate reserve asset could face its toughest test yet. For now, the data suggests that the "Saylor Sell-off" was a psychological event rather than a liquidity event. The real story remains the $4.4 billion moving out of ETFs and the shifting geopolitical landscape, both of which dwarf the tactical movements of a single corporate treasury.