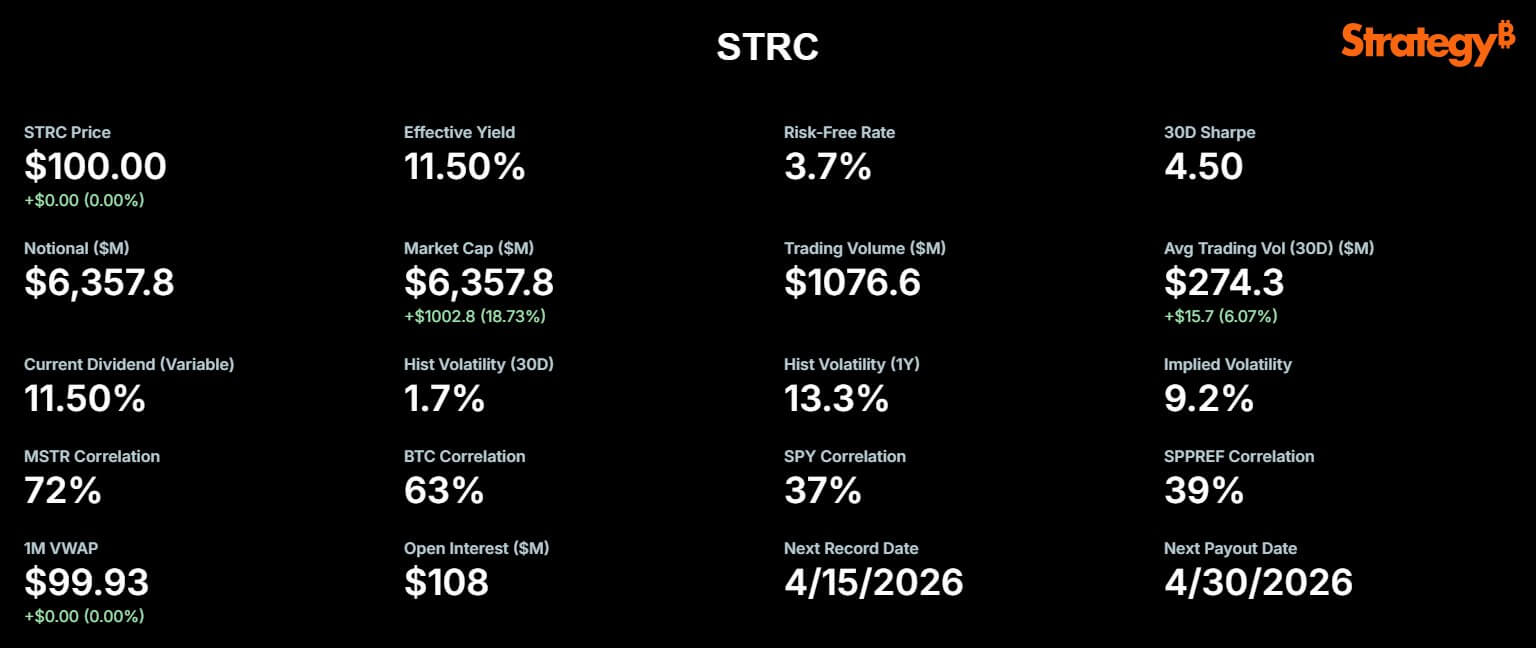

Strategy’s perpetual preferred stock, trading under the ticker STRC, emerged as a cornerstone of the firm’s aggressive digital asset acquisition framework this week, recording a staggering daily trading volume exceeding $1.1 billion. This surge in liquidity coincides with a pivot in the company’s capital allocation strategy, marking a transition toward utilizing sophisticated fixed-income instruments to fund its multi-billion-dollar Bitcoin treasury. Michael Saylor, the company’s Executive Chairman, confirmed via social media that on April 13, the security moved $1.156 billion in market liquidity while maintaining exceptional price stability, closing at par with what he described as a mere “one penny of volatility.”

The record-breaking trading activity follows a high-stakes acquisition period between April 6 and April 12, during which Strategy purchased 13,927 Bitcoin for approximately $1 billion. This transaction has further solidified the company’s position as the largest corporate holder of the cryptocurrency. With the latest purchase integrated into its balance sheet, Strategy now oversees a total treasury of 780,897 Bitcoin. The cumulative acquisition cost for this digital hoard stands at $59.02 billion, representing an average purchase price of $75,577 per coin.

The Evolution of the STRC Funding Mechanism

The recent $1 billion acquisition was funded entirely through the company’s at-the-market (ATM) issuance program, specifically involving the sale of 10.02 million STRC shares. By generating approximately $1 billion in net proceeds through this method, Strategy has demonstrated a significant shift in how it interacts with capital markets. Historically, the firm relied heavily on common stock issuance and convertible senior notes; however, the emergence of the STRC preferred stock program indicates a more nuanced approach to balance sheet management.

Launched in July 2025, the STRC security was engineered to provide a distinct alternative to the company’s MSTR common stock. Unlike common equity, which fluctuates wildly based on the underlying price of Bitcoin and market sentiment, STRC is designed to trade near its $100 par value. To achieve this stability, the instrument carries a variable annualized dividend rate, which as of April stands at 11.50%. This high-yield, adjustable-rate structure serves a dual purpose: it incentivizes investors to provide deep liquidity and ensures the stock remains an attractive vehicle for income-oriented institutional funds that might otherwise avoid the volatility of pure-play cryptocurrency investments.

Strategic Implications for the Capital Structure

For equity investors, the shift toward preferred stock as a primary funding engine represents a double-edged sword. On one hand, the use of STRC can mitigate the immediate dilutive impact on common shareholders. When the company issues preferred shares instead of common shares, the total number of ordinary shares remains stable, preventing the "per-share" value of Bitcoin holdings from being spread too thin.

On the other hand, preferred stock introduces a layer of "fixed claims" that sit ahead of common equity in the corporate hierarchy. In the event of a financial restructuring or liquidation, STRC holders must be paid in full before common shareholders receive any residual value. Furthermore, the 11.50% dividend represents a mandatory cash outflow that the company must service regardless of its operational profitability. This creates a "leverage effect": if Bitcoin’s price appreciates significantly faster than the cost of servicing the dividend, common shareholders reap amplified rewards. Conversely, if Bitcoin’s price stagnates or declines, the burden of the preferred dividend could erode the company’s cash reserves and pressure the value of common equity.

Chronology of Strategy’s Bitcoin Expansion

The trajectory of Strategy’s Bitcoin journey has moved from experimental treasury management to a systemic financial operation. To understand the significance of the recent $1.1 billion STRC volume, one must look at the timeline of the company’s recent milestones:

- July 2025: Strategy launches the STRC perpetual preferred stock, aiming to tap into the $7 trillion traditional income fund market.

- February 2026: The company establishes a $2.25 billion financial reserve. This move was a preemptive strike against critics who questioned the firm’s ability to pay dividends given that its core software business does not generate enough cash flow to cover the high yield of the STRC program.

- February – March 2026: STRC’s market capitalization begins a rapid ascent, nearly doubling from $3.4 billion to over $6 billion as institutional appetite for "Digital Credit" grows.

- April 6–12, 2026: Strategy executes a $1 billion Bitcoin purchase, its largest single-week acquisition funded exclusively through preferred stock ATM sales.

- April 13, 2026: STRC records historic daily volume of $1.156 billion, proving the depth of the secondary market for the security.

As of today, the STRC market capitalization has reached approximately $6.36 billion. Despite this rapid growth, the company still has a significant runway, with $21.6 billion worth of STRC shares still authorized for future issuance under its current shelf registration.

Analyzing the "Digital Credit" vs. "Digital Kamikaze" Debate

The rapid expansion of the STRC program has divided the analyst community into two distinct camps. Supporters, such as Bitcoin analyst Adam Livingston, view STRC as a "machine" that converts traditional capital market access into long-duration Bitcoin exposure. Livingston argues that the model is inherently accretive because the fixed claim of the preferred stock becomes smaller and smaller relative to the total asset base as Bitcoin continues its long-term compounding.

Michael Saylor has reinforced this bullish outlook, stating that the company’s Bitcoin Breakeven Accounting Rate of Return (ARR) is approximately 2.05%. According to Saylor’s logic, if the value of the company’s Bitcoin holdings grows by more than 2.05% annually, the firm can theoretically cover its dividend obligations indefinitely without ever needing to sell Bitcoin or dilute common shareholders further.

However, skeptics like independent analyst Derin Olenik offer a much grimmer assessment. Olenik’s research suggests that the current rate of STRC issuance is unsustainable. He points out that the notional value of the company’s obligations is growing at a compound monthly rate of roughly 30%. At this pace, the financial pressure on the company’s reserves could escalate ten-fold within a single year.

Olenik warns that Strategy’s $2.25 billion reserve, originally intended to last 2.5 years, could be depleted in as little as nine to ten months if the current pace of acquisition and dividend payouts continues. If the reserve runs dry and the company cannot access new financing, it would be forced into a "hyper-dilution" scenario. Olenik estimates that the company might need to issue over one billion new common shares to meet its preferred obligations, potentially diluting existing equity by as much as 400%. For this reason, Olenik famously labeled the STRC instrument as "Digital Kamikaze" rather than "Digital Credit."

The Role of the $2.25 Billion Reserve

Central to the company’s survival in this high-yield environment is the $2.25 billion cash reserve established in early February. Because Strategy’s legacy software business remains a secondary priority compared to its Bitcoin development activities, the operating income is insufficient to meet the hundreds of millions of dollars in annual dividend payments required by the STRC program.

The reserve acts as a "buffer" or a "runway." It is designed to reassure investors that even in a prolonged Bitcoin bear market or a period of high interest rates, the company has the liquidity to honor its commitments to preferred shareholders for at least 30 months. The sustainability of this model relies on three variables: the continued ability to sell STRC shares at par, the price appreciation of Bitcoin, and the ability to replenish the reserve through future capital raises or asset-backed lending.

Broader Market Impact and Future Outlook

The success of the STRC program is being closely watched by Wall Street as a potential blueprint for other corporations. By creating a high-yield instrument backed by the perceived long-term value of Bitcoin, Strategy has effectively created a new asset class: Bitcoin-collateralized corporate credit.

For MSTR common shareholders, the path forward is one of extreme volatility and high stakes. The company has essentially leveraged its balance sheet to the maximum extent permitted by current market conditions. If Michael Saylor’s vision of Bitcoin as a "pristine collateral" holds true, the STRC program will be remembered as a masterstroke of financial engineering that allowed the company to acquire nearly 800,000 BTC with minimal equity dilution.

However, the risks remain systemic. The company’s reliance on continuous market access means that any freeze in the credit markets or a significant regulatory crackdown on digital asset-linked securities could jeopardize the entire structure. For now, the $1.1 billion in trading volume suggests that institutional confidence remains robust, but the "math of hyper-dilution" highlighted by critics remains a lingering shadow over the company’s long-term prospects. As Strategy continues to push toward its goal of holding one million Bitcoin, the STRC preferred stock will undoubtedly remain the most critical, and most controversial, tool in its arsenal.