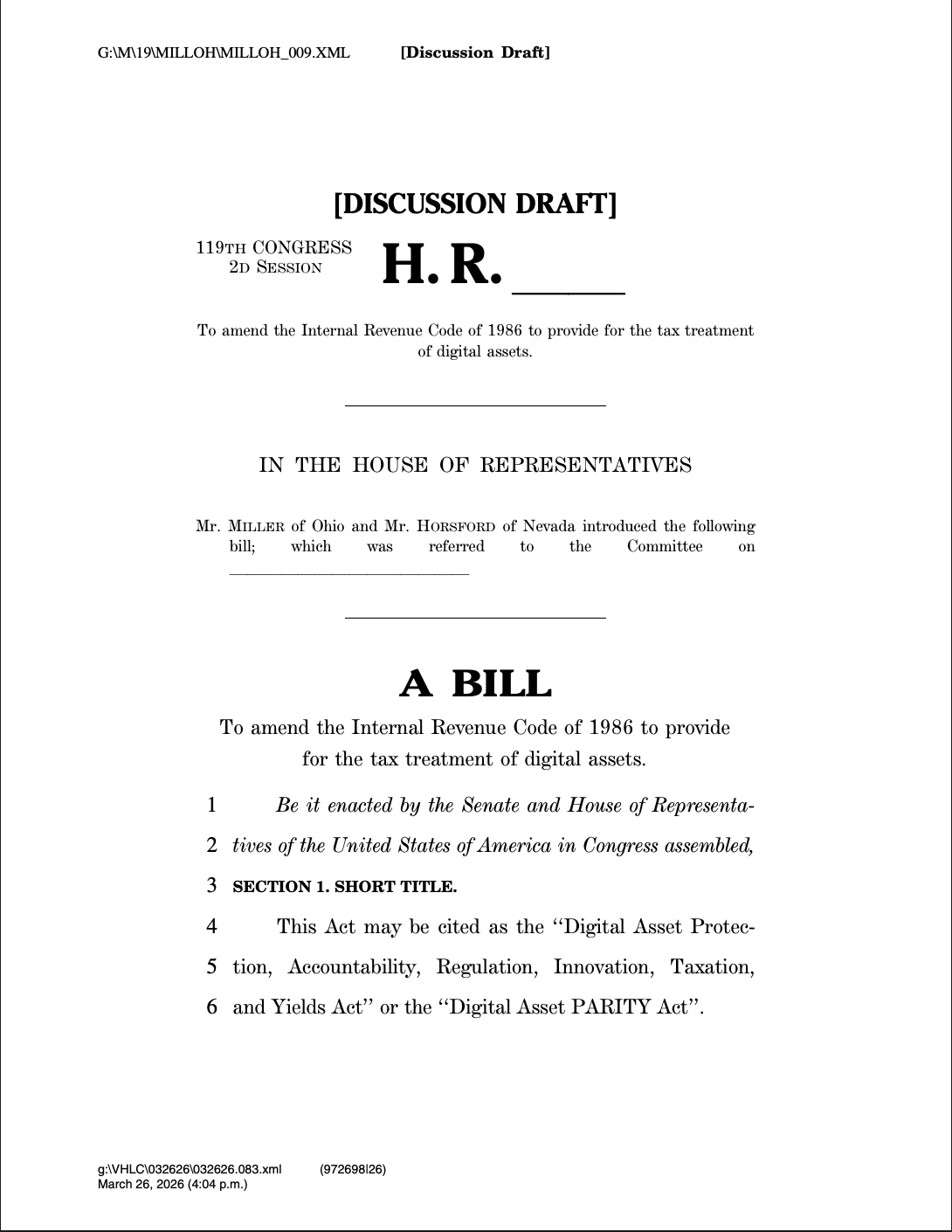

In a significant move towards establishing comprehensive regulatory clarity for the burgeoning digital asset sector, U.S. Representatives Max Miller (R-OH) and Steven Horsford (D-NV) unveiled a discussion draft bill on Thursday, christened the "Digital Asset Protection, Accountability, Regulation, Innovation, Taxation, and Yields Act," more concisely known as the "Digital Asset PARITY Act." This bipartisan legislative proposal aims to fundamentally overhaul the existing tax code as it applies to digital assets, addressing a long-standing demand from industry stakeholders for clearer guidance and a more predictable operational environment. The draft’s release signals a critical juncture in the ongoing legislative debate surrounding how digital assets should be integrated into the traditional financial and tax frameworks of the United States.

Core Provisions of the Digital Asset PARITY Act Discussion Draft

At its heart, the Digital Asset PARITY Act seeks to amend the Internal Revenue Code of 1986 by introducing specific provisions designed to clarify the tax treatment of various digital assets. The proposed changes are particularly focused on stablecoins and the income generated from common decentralized finance (DeFi) activities like lending and staking.

One of the most notable provisions pertains to stablecoins. The legislation outlines that stablecoins, particularly those pegged to the U.S. dollar, would not be subject to capital gains taxes under specific conditions. This exemption would apply if the cost basis, which is the initial amount paid by the investor, does not fluctuate by more than 1% of $1, or $0.01. This aims to recognize the unique nature of stablecoins, which are designed to maintain a stable value relative to a fiat currency, and differentiate them from more volatile cryptocurrencies like Bitcoin or Ethereum. Furthermore, the draft specifies that transaction costs incurred when acquiring or moving regulated dollar-pegged stablecoins cannot be factored into an investor’s cost basis. This provision seeks to streamline the tax treatment of stablecoin usage, potentially encouraging their adoption for everyday transactions by reducing the complexity of tracking minor cost adjustments.

Adding to the stablecoin-centric focus, the bill introduces a crucial de minimis tax exemption for stablecoin transactions. Under this proposed rule, stablecoin transactions below a threshold of $200 would not trigger tax liabilities or reporting requirements. This is a significant development, as current tax law often treats every crypto transaction as a taxable event, requiring meticulous record-keeping even for small purchases or transfers. While the discussion draft sets the individual transaction threshold at $200, an overarching annual exemption cap for such transactions is yet to be determined, indicating an area for further deliberation and stakeholder input. The intent behind this de minimis exemption is to remove a significant barrier to the practical use of stablecoins for payments and micro-transactions, aligning their tax treatment more closely with traditional fiat currencies for small-value exchanges.

Beyond stablecoins, the Digital Asset PARITY Act also addresses the taxation of income derived from various digital asset activities. Income generated from lending, staking, or earned through "passive" validator services would be treated as part of the recipient’s gross income annually. This income would be calculated using its "fair market value" at the time it is received. This clarification is vital for participants in the rapidly growing DeFi ecosystem, where earning yield through staking or lending digital assets has become commonplace. By explicitly defining how such income should be taxed, the bill aims to provide much-needed certainty for investors and platforms alike, mitigating ambiguity that has previously led to compliance challenges.

It is crucial to underscore that the Digital Asset PARITY Act currently exists as a discussion draft. It has not yet been formally introduced to Congress for legislative consideration. Its publication serves as an open invitation for debate and feedback from lawmakers, industry stakeholders, crypto advocates, and the broader public. This approach allows for refinement and consensus-building before the bill potentially moves through the legislative process, reflecting a deliberate effort to craft well-informed and broadly supported crypto tax policy in the United States.

Background and the Quest for Crypto Tax Clarity

The introduction of the Digital Asset PARITY Act comes against a backdrop of increasing calls for regulatory clarity in the U.S. digital asset space. For years, the Internal Revenue Service (IRS) has largely treated cryptocurrencies as property for tax purposes, a classification established in its 2014 guidance. While this guidance provided an initial framework, it has proven increasingly inadequate for the rapidly evolving and complex digital asset ecosystem, which now includes a diverse array of assets from volatile cryptocurrencies to stablecoins, NFTs, and various DeFi protocols.

The "property" classification means that every transaction involving a digital asset—whether it’s selling, trading for another crypto, or using it to purchase goods and services—can potentially be a taxable event, triggering capital gains or losses. This has created immense compliance burdens for everyday users and professional traders alike, necessitating sophisticated tracking software and extensive record-keeping. The absence of a de minimis exemption for general crypto transactions, unlike many foreign currencies or small stock trades, has been a particular point of contention, stifling micro-transactions and practical utility.

Past legislative efforts and discussions have frequently highlighted the need for reform. The Infrastructure Investment and Jobs Act of 2021, for instance, included controversial provisions expanding reporting requirements for "brokers" in the digital asset space, stirring debate over who qualifies as a broker and the feasibility of implementing such rules. Other proposed bills, such as the Lummis-Gillibrand Responsible Financial Innovation Act and various iterations of market structure bills like the CLARITY Act, have also sought to bring comprehensive regulatory frameworks to digital assets, often including tax provisions. However, a unified and detailed approach to crypto taxation, particularly addressing common activities like staking and stablecoin usage, has remained elusive.

The U.S. digital asset market has grown exponentially, with millions of Americans now owning, trading, or interacting with cryptocurrencies. The global market capitalization of cryptocurrencies has fluctuated significantly but has at times exceeded trillions of dollars, with the U.S. being a major hub for innovation and investment. This growth has amplified the urgency for clear tax rules, as businesses struggle with compliance uncertainties and investors face potential penalties due to complex and ambiguous regulations. Lawmakers like Representatives Miller and Horsford recognize that a lack of clear rules risks driving innovation and economic activity offshore, undermining the U.S.’s competitive edge in the digital economy. Industry advocacy groups, such as the Digital Chamber, have consistently lobbied Congress for clearer guidelines, emphasizing that regulatory certainty is a prerequisite for mainstream adoption and robust domestic growth.

Supporting Data and Economic Implications

The potential economic implications of clear digital asset tax policy, as envisioned by the PARITY Act, are substantial.

- Market Scale: The digital asset market represents a significant and growing segment of the global economy. While exact figures fluctuate, estimates suggest that tens of millions of Americans own some form of cryptocurrency. According to a 2023 survey by Statista, approximately 26% of adults in the United States reported owning cryptocurrencies. This widespread adoption underscores the necessity of a clear tax framework that can accommodate diverse users and use cases.

- Innovation and "Onshoring": Cody Carbone, CEO of the crypto advocacy organization Digital Chamber, succinctly articulated the industry’s perspective, stating, "We need digital asset tax clarity or activity will never fully onshore." This sentiment reflects a broader concern that without a predictable regulatory environment, businesses and innovators in the digital asset space might opt to establish operations in jurisdictions with more defined rules, potentially leading to a "brain drain" and economic loss for the U.S. The PARITY Act, by providing specific tax guidance, aims to create an environment where digital asset companies feel confident operating and investing within the U.S. borders.

- Reducing Compliance Burden: The current tax framework often imposes significant compliance burdens on individual investors and businesses. Every transaction, no matter how small, can be a taxable event. For someone who uses a stablecoin for a daily coffee purchase, tracking the cost basis and potential gains (even if minimal) can be a daunting task. The proposed de minimis exemption for stablecoins below $200 directly addresses this pain point, simplifying reporting for routine transactions and potentially encouraging the use of stablecoins for payments, which could foster greater economic activity.

- Revenue Generation: While simplifying taxes for small transactions, the bill also aims to ensure that significant income from digital asset activities, such as staking and lending, is properly reported and taxed. By defining these income streams as gross income calculated at fair market value, the IRS can more effectively collect revenue from a growing segment of the financial landscape, contributing to the nation’s tax base.

- Consumer Protection and Education: Clear tax rules also serve as a form of consumer protection. When investors understand their obligations, they are better equipped to make informed decisions and avoid unintentional non-compliance, which can lead to penalties. The act’s focus on clarity can help educate the public on the tax implications of their digital asset activities.

Stakeholder Reactions and the Industry Schism

The release of the Digital Asset PARITY Act discussion draft has predictably elicited a range of reactions, highlighting a significant "schism" within the broader crypto industry regarding legislative priorities and philosophical approaches to digital assets.

On one side, proponents of the bill and broader regulatory clarity, often represented by established crypto advocacy groups, view the draft as a positive step. Cody Carbone’s statement about the need for clarity to "onshore" activity exemplifies this view. For many in the industry, any move towards detailed, specific tax guidance is welcomed, as it provides the certainty needed to innovate, attract investment, and operate within the U.S. legal framework. Stablecoin issuers, in particular, are likely to view the proposed de minimis exemption and clarified tax treatment favorably, as it could significantly boost the utility and adoption of their products for everyday transactions. Platforms offering staking and lending services would also benefit from explicit rules, which could reduce their own compliance risks and allow them to better advise their users.

However, the draft has also drawn criticism from a segment of the crypto community, particularly those aligned with "Bitcoin Maximalist" principles. Pierre Rochard, CEO of The Bitcoin Bond Company, voiced strong opposition, stating, "This is the wrong direction to go in." His primary contention revolves around the selective nature of the de minimis tax exemption, which is proposed for stablecoins but notably excludes Bitcoin (BTC) and other more volatile cryptocurrencies.

Rochard articulated a common argument among Bitcoiners: "It’s Bitcoin that should have a de minimis tax exemption. Stablecoins are not decentralized, and they are not permissionless. They’re not real money; they’re just fiat." This perspective highlights a fundamental philosophical divide. Bitcoiners often view Bitcoin as a truly decentralized, permissionless digital monetary system distinct from government-issued fiat currency or centralized stablecoins, which they see as extensions of the traditional financial system. For them, Bitcoin’s unique properties warrant preferential tax treatment, particularly regarding micro-transactions, to foster its adoption as "real money." The exclusion of Bitcoin from such an exemption in the PARITY Act is therefore seen as a misstep that prioritizes centralized digital assets over genuinely decentralized ones. This mirrors similar concerns raised about other pending legislation, such as the CLARITY crypto market structure bill, which also lacks a BTC de minimis tax exemption.

From a regulatory enforcement perspective, the IRS and Treasury Department would likely welcome the additional clarity provided by the PARITY Act. While new rules can introduce administrative burdens, clear statutory guidance simplifies enforcement, reduces litigation risks, and ensures more equitable tax collection. Policymakers, generally, are grappling with the complexities of digital assets, and bipartisan efforts like the PARITY Act signal a growing recognition of the need for collaborative solutions.

Broader Impact and Future Legislative Pathway

The introduction of the Digital Asset PARITY Act discussion draft marks a crucial inflection point in the U.S. journey toward comprehensive digital asset regulation. Its ultimate impact, should it progress to become law, could be far-reaching, affecting investors, businesses, and the very trajectory of innovation in the crypto space.

The proposed de minimis exemption for stablecoins, if enacted, could dramatically simplify the tax experience for users engaging in small-value transactions. This could significantly lower the barrier to entry for mainstream adoption of stablecoins for payments, potentially fostering a new wave of economic activity in the digital realm. Businesses that accept stablecoins would also benefit from reduced reporting complexities, making digital asset integration more attractive. However, the absence of a similar exemption for Bitcoin and other cryptocurrencies will likely continue to fuel debate and advocacy from their respective communities, potentially leading to further legislative proposals.

For those involved in staking and lending, the explicit classification of such income as gross income, valued at fair market value, provides much-needed legal certainty. While this means these activities will clearly be taxable, the clarity allows individuals and platforms to plan and comply effectively, reducing the risk of unexpected tax liabilities. This could also encourage the development of tax-compliant DeFi products and services within the U.S.

The legislative pathway for the Digital Asset PARITY Act will be complex and potentially lengthy. As a discussion draft, it is currently in its nascent stage. The next steps would involve soliciting feedback, likely through public comment periods, congressional hearings, and stakeholder meetings. Based on this input, Representatives Miller and Horsford, or other sponsors, would then refine the draft and formally introduce it as a bill in either the House or Senate. From there, it would need to pass through relevant committees, potentially undergo further amendments, and then be approved by both chambers of Congress before being sent to the President for signature. This process is inherently political and subject to various influences, including lobbying efforts from different segments of the crypto industry, the broader financial sector, and consumer advocacy groups.

The bipartisan nature of this draft is a positive indicator, suggesting that there is common ground across the political spectrum on the necessity of addressing digital asset taxation. However, the differing views on specific provisions, particularly the scope of de minimis exemptions, underscore the challenges in crafting legislation that satisfies all stakeholders in such a diverse and rapidly evolving sector. The ongoing debate around the PARITY Act will undoubtedly contribute to the larger conversation about how the U.S. plans to regulate digital assets, balancing the goals of fostering innovation, protecting consumers and investors, ensuring financial stability, and maintaining a fair and efficient tax system. The outcome of this legislative effort could set a precedent for future digital asset policies, shaping the future of crypto in America for years to come.